Reports are for crop conditions up to May 3, 2024.

Western Maryland

April has brought us many showers. The triticale is all in the silos for the most part, and corn planting has begun. The wheat and the barley are looking good. Producers have a keen eye out for FHB, and thus, fungicide is on the docket. Pastures are looking good and first cutting alfalfa is not far off. Warmer temperatures are on the horizon.—Jeff Semler, Washington Co.

Central Maryland

The wet, cool spring has turned into a hot, dry spring this week. Currently, the highest chance of rain (about 60%) is for this weekend. Planting is in full swing, and the first cutting of orchardgrass will start in a couple weeks. Wheat and barley are heading; if the drier weather keeps up, it will lower the risk for Fusarium.—Kelly Nichols, Montgomery Co.

Northern Maryland

Rain has been hard to come by with only about 1” of accumulated rain in the last 4 weeks. Corn and soybean planting has been in rolling for 2.5 weeks now, with a very large majority of it within the last week to 10 days or so. Small grains generally look very good, pastures and hay fields have also enjoyed the cooler than normal March and April. Wheat is anywhere from boot to head emergence. After a soggy start to April, we could use some rain.—Andy Kness, Harford Co.

Upper and Mid Shore

The rains from early in the month are now just a memory, with clear skies and no significant rainfall since. Dust clouds swirling on the horizon are a clear sign that #Plant2024 is underway. Farmers are terminating their cover crops and tilling the soil, readying it for planting. This year, we’re running a week or two ahead of last year’s schedule, raising hopes for another bumper crop. Small grains are currently heading, with some currently flowering.—Dwayne Joseph, Kent Co.

Lower Shore

After a rainy stretch, we’ve gotten some dry weather this past week. About half or more of cover crop acreage has been terminated. Some ground is being tilled, while the majority will be planted no-till. Corn is currently being planted. Wheat is looking very good. If wheat varieties are susceptible to Fusarium Head Blight and if the wheat is flowering, fungicides should be considered. The first cutting of hay has started.—Sarah Hirsh, Somerset Co.

Southern Maryland

Field conditions are a mixed bag. Areas to the north have turned dry in the last week. Areas to the south received more rain delaying field operations. In drier areas, soil has become hard and compacted, aggravated by wet conditions over the winter. This is a year where big differences in soil conditions can be observed between no-till and tilled fields. Planters have been rolling for the last two weeks with conditions mostly ideal for planting. Corn emergence looks good so far. Slugs were a concern early, but drier weather has helped with that issue. We have many acres of early planted soybeans again this year. Burndown programs have been challenged this year with many escapes of annual ryegrass. Wheat is headed and beginning to flower now. We are observing some yellowing of the flag leaf and leaf below the flag leaf across many fields that showed up in the last 10 days. We are working to determine the exact cause, but believe it related to environmental conditions with perhaps some virus issues like BYDV as well. A lot of good dry hay has been made in the last two weeks. On the fruit and vegetable front, plasticulture strawberries look very good and are ripening now. All of our main season vegetable crops are preparing to go in the ground this week. High tunnel crops are coming off now.—Ben Beale, St. Mary’s Co.

Andrew Kness, Senior Agriculture Agent | akness@umd.edu and Nidhi Rawat, Small Grains Pathologist University of Maryland

Over the past couple of weeks we have gotten several questions about yellowing flag leaves on wheat. Generally these symptoms are appearing widespread in fields. To the best of our knowledge we can attribute this to leaf burn or leaf tip necrosis (LTN) (Figure 1). This disorder is often a response to cold injury or wind, but can also manifest as a result of heat and drought stress. We have had widespread hot and dry conditions for several weeks across Maryland, which can trigger these symptoms, especially on lighter soils. These symptoms can also be intensified by specific leaf rust and stripe rust resistance genes and LTN severity can vary greatly between varieties. In any case, there is nothing you can do to remedy the situation.

Figure 1. Wheat leaves with symptoms of leaf tip necrosis. Note the dead tissue at the leaf tips.

Leaf tip necrosis may be confused with barley yellow dwarf virus (BYDV). BYDV is undoubtedly contributing to some of the symptoms in many of these fields, but it is probably not the sole factor causing these symptoms. LTN tends to cause death of the leaf tip resulting in necrotic brown tissue (Figure 1), whereas BYDV can cause a range of symptoms from yellowing of the leaf, which may or may not be accompanied with bronzing/purpling of the leaf tips (Figure 2). Notably with BYD, leaf tips do not die and become necrotic; whereas leaf tissue from LTN will become brown and dead starting at the leaf margins near the tip and work inward. Since BYDV is vectored by aphids, symptoms tend to be localized in hotspots in a field where aphids populations are high, whereas leaf burn and LTN more uniformly affect the entire field.

Figure 2. Symptoms of barley yellow dwarf virus. Leaf tips are yellow and purple/bronze but tissue is not dead.

Andrew Kness, Senior Agriculture Agent | akness@umd.edu University of Maryland Extension, Harford County

This article may come a little too late for some of you depending where you are in the state; but nevertheless, here is a review/reminder. As we get into May, wheat will begin flowering and we will have to consider fungicide applications to wheat to manage Fusarium head blight (FHB), also known as head scab. FHB is the most economically important disease of wheat, causing not only yield reductions, but more seriously, grain quality issues due to the production of the mycotoxin deoxynivalenol (DON), also called vomitoxin.

The pathogen that causes FHB, Fusarium graminearum, persists in wheat, small grain, and corn residue. It infects the wheat plant through the open flower, which is why flowering is such an important management timing for quality wheat production. Fusarium graminearum requires moist conditions and moderate temperatures (59-86 °F) to initiate infection. If these conditions are met during flowering, the pathogen will infect susceptible wheat varieties and cause disease.

Management of FHB requires a layered approach of IPM practices, with the major management practices being the selection of a good wheat variety and subsequent good planting and fertility practices, plus the use of a fungicide at flowering should the environmental conditions be conducive for FHB development. The wheatscab.psu.edu map can be helpful in predicting FHB risk to wheat around flowering. Historically, this model has been over 70% effective at predicting FHB outbreaks and should be consulted when making fungicide decisions. If you decide to apply a fungicide to manage FHB, there are three important factors to consider: 1.) Timing, 2.) Application method, and 3.) Active ingredient.

As mentioned earlier, the pathogen can only infect wheat through the open flower, so you need to time your fungicide application as close to flowering, or Feekes Growth Stage 10.5.1, as possible (Figure 1). This growth stage is defined by the appearance of yellow anthers in the center of the wheat spike on at least 50% of the plants. Once this stage is reached, the application window is about 5-7 days. Some fungicide products are labelled for application as early as Feekes 10.3 (half head emergence); however, this timing is not as optimal as 10.5.1—so wait if you can.

Figure 1. Wheat at Feekes 10.5.1, indicating proper fungicide timing for FHB management. Photo: A. Kness, Univ. of Maryland.

The second factor is application method. Most of our fungicides on wheat go on with a ground sprayer. For ground applications it is important to achieve good coverage of the wheat heads, not the foliage. To do this, spray volumes should be at least 15-20 gallons/acre and you should use bi-directional spray nozzles angled forward and backwards. This combination of spray volume and angled nozzles results in thorough coverage of the wheat heads. Aerial applications should be done at 5 gallons/acre for maximum coverage.

The final consideration is fungicide active ingredient. Triazole and HDMI fungicides work best on FHB. Products include: Prosaro Pro, Prosaro, Miravis Ace, Saphaerex, Proline, and Caramba; Folicur has less efficacy than the others and Tilt is no longer effective on FHB. An added benefit is that these products will also do a good job of keeping other fungal diseases at bay during grain fill. Do not apply any group 11 (Qoi/strobilurin) fungicides such as Aproach, Headline, or Quadris after heading as these products can actually increase DON levels in the grain.

Nidhi Rawat, Small Grains Pathologist University of Maryland, College Park

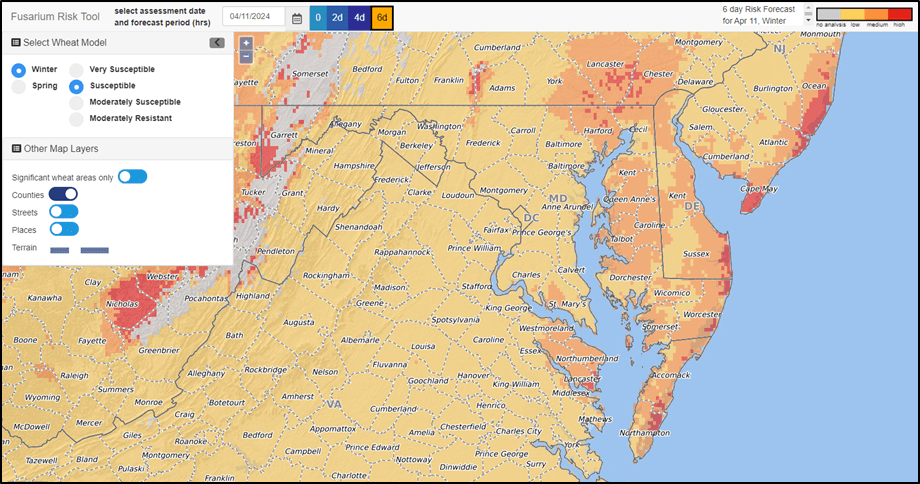

Wheat is currently flowering or will soon flower across the state of Maryland. Flowering is when yellow anthers emerge out of the wheat spikes. This is again that year, in which if you planted a resistant variety, you would be okay without spraying fungicides for controlling Fusarium head Blight (FHB risk map: top picture). However, if your planted variety is not FHB resistant, you should consider application of FHB fungicides (FHB risk map: lower picture). If you are planning to apply fungicides for FHB, remember that triazole-containing fungicides (Miravis-Ace, Prosaro, Prosaro-Pro, and Sphaerex) should be used for controlling FHB. They can control other fungal pathogens like powdery mildew, rusts, in addition to scab. Strobilurin-containing fungicides should not be used at this stage. These fungicides do not need to be tank mixed with another product for spraying. The fungicide products should be applied at the full rate recommended by the manufacturers. Aerial application at a rate of 5 gallons per acre or ground application at 15 gallons per acre with 300-350 um droplet size is recommended. Spray nozzles should be angled at 30°-45° down from horizontal, toward the grain heads, using forward- and backward-mounted nozzles or nozzles with a two directional spray, such as Twinjet nozzles.

Nidhi Rawat, Small Grains Pathologist University of Maryland, College Park

Wheat on the Eastern shore of Maryland is heading and should start flowering within a week or so. Wheat in the north-western part (Frederick, Carroll, Hartford counties) is also close to heading or has started heading. The FHB fungal pathogen infects the wheat plants at the flowering stage (when the yellow anthers emerge from the heads), which is the stage at which the application of fungicides is conducted in wheat. The FHB map currently does not show high risk, especially for a genetically resistant variety. However, keeping an eye on the forecasts and weather patterns over the next few days as your wheat flowers is recommended. If you are planning to apply fungicides for FHB, remember that triazole-containing fungicides (Miravis-Ace, Prosaro, Prosaro-Pro, and Sphaerex) should be used for controlling FHB. They can control other fungal pathogens like powdery mildew as well, in addition to scab. Strobilurin-containing fungicides should not be used at this stage.

Nidhi Rawat, Small Grains Pathologist University of Maryland

Welcome to the wheat and barley heading and flowering season, Maryland! This is the first FHB risk forecast for this season from me, and I will continue to provide you with regular commentaries over the next 6-7 weeks. Wheat is some weeks away from flowering, but barley is starting/ will soon start to head, especially in the Eastern shore of the state. Unfortunately, for barley, there are no FHB-resistant varieties available so far. So, if you have planted barley, keep monitoring closely for the FHB risk over the next couple of weeks. With the rainy spell of the last week, and some more rain forecasted this week, currently, the Epidemiological models are showing elevated FHB risk over the next 6 days. So, if your barley is starting heading you might consider applying fungicides on it. If you are still some weeks away from your barley heading, keep monitoring for the risk. Remember, the best stage for applying FHB fungicides on barley is when the heads are completely out of the boots. The FHB fungicides are triazole-containing products (Miravis-Ace, Prosaro, Prosaro-Pro, Sphaerex). Do not apply strobilurin-containing fungicides after heading. Wheat is not at a stage susceptible to FHB right now.

Some barley growers from across the state reported stunting, yellowing, and death of barley plants in their fields. The most probable cause of this issue in my opinion is freeze injury. Sudden dips in temperature after the plants caught up after winter may have led to the issue. I have discussed this issue with the other regional pathologists from the US, and they also report similar issues in North Carolina, Pennsylvania, and New York. They also think it to be a result of cold injury.

Mark Townsend, Agriculture Agent Associate | mtownsen@umd.edu University of Maryland Extension, Frederick County

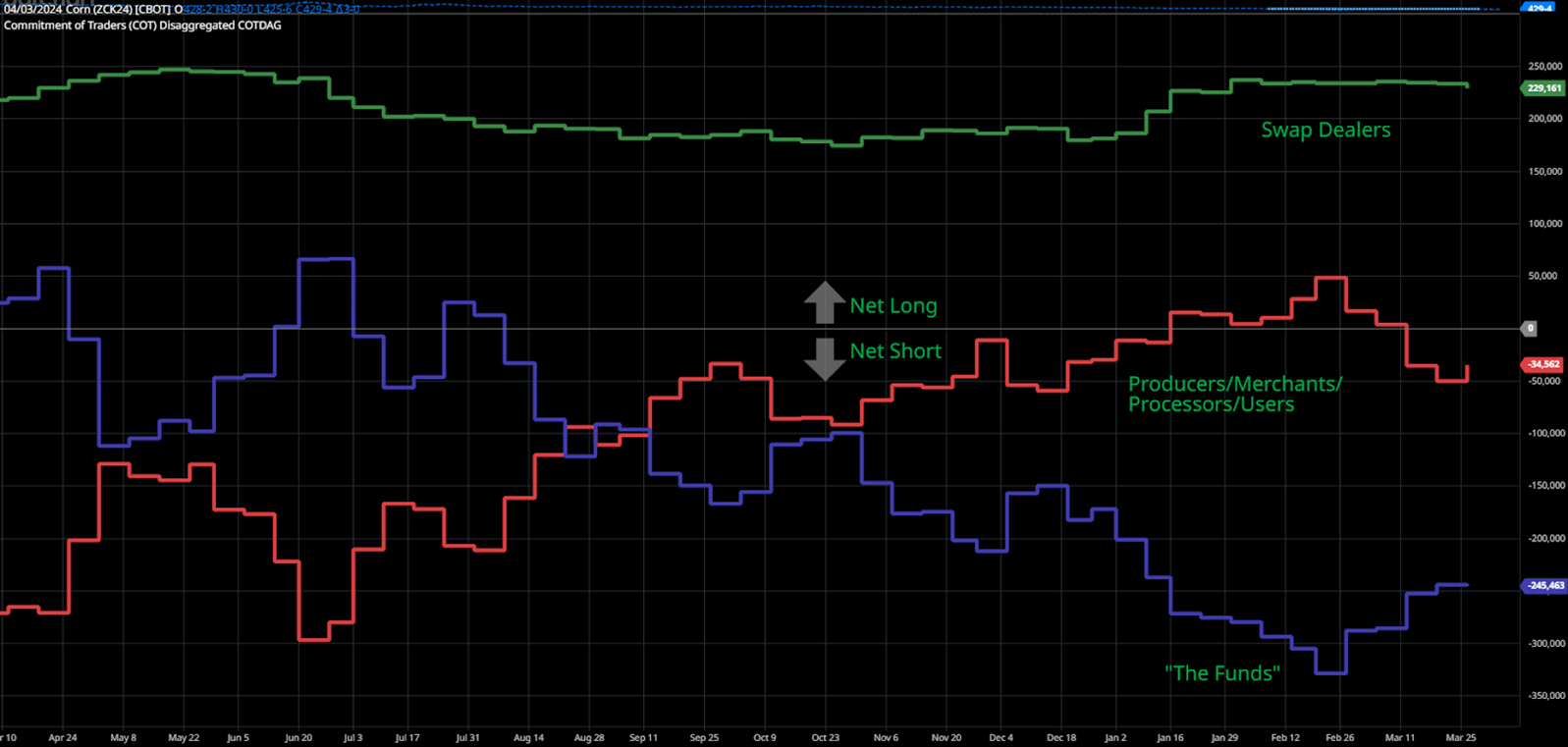

Grain markets have slid significantly from the highs posted last summer that followed the perceived drought in the Midwest.

Image Credit: Barchart: December ‘24 Corn Contract from June 2023 to April 3, 2024.

Unfortunately, these drought concerns were generally unfounded as key growing areas received timely rains to keep yields from suffering in the corn belt. In fact, the U.S. set a new corn production record at 15.234 billion bushels topping the previous record set in 2016 at 15.148 billion bushels. The trifecta of a record large U.S. crop, a large Brazilian corn crop, as well as underwhelming domestic and export demand sent prices spiraling lower from August 2023 to February 2024. The March ‘24 Corn contract traded at three-year lows on February 26th dipping below $4 following 11 consecutive week-over-week price declines.

Soybeans were unfortunately no better, falling $2.90 from their summer high ($14.18) to their low ($11.28) in the March ‘24 contract. Much of the same stories plagued this market including an unrealized weather rally and outstandingly large South American production that punished U.S. export demand.

To add insult to injury, “the Funds”—traders in the market who manage money for clients as either hedges or other investment strategies hit a record 340,732 net short position in the corn market on February 20th. Simply stated, these traders placed the largest-ever bet on corn prices continuing to decline, which has placed a metaphorical wet-blanket on any hopes of a rally.

Today

Grains have rallied from the end of February and throughout March. The inflection point was the last day of notice for March hedge-to-arrive (HTA) contracts. To that point, sellers (farmers, dealers, etc.) had the choice of pricing corn at current prices or “rolling” the contract to the May contract. The bleak outlook forced many hands and stimulated selling which pulled prices lower until the selling pressure was over.

Since then, both the corn and soybean markets have rallied off the lows and recovered to price levels previously seen in early February. The upward momentum has been driven by a phenomenon known as “short covering” that creates a positive feedback loop–the more it happens, the more it happens. As prices rise, “The Funds” in their net short position lose money as their bet has turned against them. To stop this, they must exit their position by buying a contract to offset the one they previously sold1. The buying stimulates further price increases that induce another fund manager having to offset their short position. At its extreme, this feedback loop can throw prices to astronomical levels2. In this case, the bump is a welcomed change but is unlikely to send us much higher for now.

More recently, the USDA released its Prospective Plantings Report compiled from surveys asking farmers their planting intentions this season. The report suggests growers will plant 90 million acres of corn and 86 million acres of soybeans, indicating that growers are shifting acres away from corn to soybeans. This was unsurprising, however traders found this as good news as the nearby contracts in both markets traded higher the day of the report. However, traders are generally wary of this recent report given the low farmer response rate and the tendency for acreage figures to climb with subsequent USDA planting reports.

Season Outlook:

The saying, “all models are wrong, but some are useful” may hold true for commodity market predictions as well; there is a significant degree of uncertainty in any market that can render any forecast absolutely incorrect. As such, this is not meant to be a forecast but more of an observation of trends and conditions that may prove useful.

Supply and Demand Fundamentals

Image Credit: Barchart. CFTC Commitment of Traders in the Corn Market (all contracts).

Every market most fundamentally relies on the interplay between supply and demand. Currently in the grains, supply has outstripped demand. Following last year’s record crop, U.S. corn supply is almost burdensome.

A common metric that evaluates how efficiently we use the crop we grow is the Ending Stocks-to-Use (S/U) ratio derived from the USDA World Agricultural Supply and Demand Estimate (WASDE) each month. Currently, the USDA projects the 2024/25 ending stocks (that which we will not use from the crop we’re about to plant) at 2.53 billion bushels and an S/U ratio of 17.2%–a level we have not seen since the 2006 when corn traded at an average price of $2.62/bu. This current 2023/24 marketing year (ending Sept. 1, 2024) is currently pegged at 14.9% S/U ratio–well higher than the 7-10% range of the last three years and the 12.6% historical average.

The soybean side of things is only marginally better and certainly not rosy by any stretch. The current S/U ratio projection for this year’s crop is 9.9% with the current marketing year sitting at 7.6%. Both these figures are a far cry from the burdensome supplies we accrued during the 2018-2019 trade war with China (22.9% S/U) yet they signal a surplus of soybeans.

Market Movers

With the current fundamentals dreary at best, it’s pleasant to think of those things that could actually help prices higher.

Midwestern drought conditions continue to worsen throughout the growing season. US weather conditions are a significant driver of price action in the growing season–as exemplified by last year. Currently, some of the Midwest is experiencing a moderate drought, with some agronomists questioning the subsoil moisture levels before planting. Importantly, drought conditions would have to persist throughout the growing season well past planting. Generally, drought is bearish to corn in April and May as Midwest growers can plant at a breakneck pace just in time for timely rains that pull yields higher and prices lower. As evidenced by last year, corn did not rally until late-May over weather concerns and in 2012, corn did not rally until mid-June. Both these years indicate that prices will likely stay mixed until real concern over crop condition emerges during the growing season.

The South American (Brazil + Argentina) soybean production is lower than expected, improving export demand for U.S. soybeans. Soybean harvest in Brazil is nearing completion, however final production estimates remain volatile. The same is true with South American corn production: a supply-side shock could support U.S. corn prices. Brazil has completed corn planting this last week of its large safrinha corn crop. Currently, much of the key corn growing regions are in a minor drought or have experiences greater than normal rainfall. More serious and persistent crop-damaging weather events could certainly be a boon to the U.S. market.

Recently, the Federal Reserve signaled that it will likely keep the Federal Funds rate higher for longer–increasing borrowing costs. If this holds true, investors may find themselves less attracted to debt and equity markets as companies may have a more difficult time generating earnings. Instead, investors may revert back to commodities–a market often seen as a hedge against inflation–as they did in 2022. As mentioned above, this may trigger a significant unwinding of short positions which could carry the market to higher prices. Unfortunately, this is likely the most unlikely scenario for increasing commodity prices as equities soar to all time highs in recent weeks.

So What Can We Do About It?

Marketing grain in 2024 will likely be challenging on all fronts. Put another way, given the current outlook, it is incredibly unlikely that selling grain in the fall at harvest prices will be a winning strategy. Similarly, it’s unlikely that an unhedged, unpriced JFM ‘25 sale will offer anything better as there are additional storage costs involved. That said, developing a preharvest marketing strategy may very well be a key to success this marketing season. Betting on the aforementioned weather stories is hardly a marketing plan.

Like every year the first step is knowing your cost of production inside and out. Marketing opportunities will present themselves, but it will take knowing what is and what is not a good price. With today’s relatively high input costs, “yielding your way out” of low prices is more challenging than previous years. Therefore it may be more crucial than ever to make judicious agronomic decisions.

Take advantage of seasonal market patterns. Generally speaking, we see 3-6% increase in corn and soybean prices between mid-March and late-May from their post-harvest lows in January. As old crop marketing wanes, and concerns over the current year’s crop emerges (like the weather), prices rise slowly during this time. It may be best to price some grain sooner rather than later to take advantage of this general trend. Put it more directly; from May 1st to October 1st, corn prices fall more than $0.30, 74% of the time. Would you bet on something weighted 75% against you?

Track local basis. Generally, basis tends to follow broader market conditions especially when it comes to spreads between nearby and more distant contracts. Seasonal trends in basis also exist with harvest often being the low point and spring generally higher.

Keep a watchful eye on the markets this season. It may be such that prices are favorable for a day or two before they fall back lower.

Please also consider attending a University of Maryland Extension grain marketing meeting. These meetings are filled with all the above strategies, general information, and more that could help you with your marketing decisions.

Best of luck to you all. Here’s to blue skies and high prices!

Reports are for crop conditions up to April 5, 2024.

Western Maryland

Wet, wet, wet. This spring is off to a very different start than last year. Late winter and early spring have gone a long way in replenishing soil moisture and groundwater. Soil temperature and moisture will delay planting for a few weeks, but we are happy to have the moisture. Chicken litter, dairy manure, and first-pass nitrogen have been applied. These rains are now filling pits uncharacteristically. We are seeing Barley Yellow Dwarf Virus in some triticale. This is new since triticale was once thought to be resistant to everything. Next fall, we will need to think about scouting for aphids. All in all we are off to a better start than 2023.—Jeff Semler, Washington Co.

Central Maryland

We’ve had quite the up and down with the weather this month. A few days in mid-March brought highs into the 60s, but most of the month has been cooler (lows in the 30s and highs in the 50s). In the past week, areas around the region have received 2 or more inches of rain. Soil temperatures have hovered around 50 degrees F. Green-up and manure applications have gone out. Looking forward to some warmer weather next week!—Kelly Nichols, Montgomery Co.

Northern Maryland

The past week has been cool and wet, which has been the story for most of the winter/early spring thus far. Field work has been very limited due to all the rain; second shot of nitrogen on wheat and weed control is needed as soon as the weather turns. Soil temperatures are still cool and the first seeds will not be going in the ground any time soon. Cover crops and small grains are generally variable across fields and winter annual weeds have been noticeably abundant this spring.—Andy Kness, Harford Co.

Upper and Mid Shore

No report.

Lower Shore

It’s been a wet spring, which has interrupted farm activities. Many fields are waterlogged or flooded. Farmers have been applying manure as they can get into fields. Most cover crops are still growing, which has been helpful to keep the rain water in the crop fields. No corn or soybean has been planted yet.—Sarah Hirsh, Somerset Co.

Southern Maryland

Rains continue to fall with only a few days here and there suitable for field work. Farmers are practicing patience as much work remains spreading litter/manure, applying herbicides and completing field operations. If weather conditions allow, planting will commence in a couple of weeks. Soils are wet and cold at present. Small grain crops are at jointing stage. Most wheat acreage received a first application of N with the second application being made when field conditions allow. Aphids have been active in some fields. Alfalfa got off to an early start this year, and growers are encouraged to scout for alfalfa weevil which has also been active. In So MD, most populations are resistant to pyrethroids, leaving Steward as the best option. Cool season grass hayfields are greening up now. On the weed front, Virginia Pepperweed seems to be more prevalent this year. Marestail and Common Ragweed are around and need to be controlled prior to planting. Burndown applications are being made in preparation for planting. With cooler temperatures, we may struggle to kill larger Italian ryegrass, brassicas, and cereal grain with standard rates of glyphosate.—Ben Beale, St. Mary’s Co.

Shannon Dill, Principal Agriculture Agent | sdill@umd.edu University of Maryland Extension, Talbot County

The University of Maryland Extension has updated www.go.umd.edu/grainmarketing site with new input data and spray programs for the 2024 field crop budgets.

Crop Budgets

Cost of production is very important when making decisions related to your farm enterprise and grain marketing. Preliminary surveys from 2024 UME Winter Crop Production meetings report 66% of farmers believe input costs are the greatest challenges facing their farm operation. Enterprise budgets provide valuable information regarding individual enterprises on the farm. This tool enables farm managers to make decisions regarding enterprises and plan for the coming production year. An enterprise budget uses farm revenue, variable cost, fixed cost, and net income to provide a clear picture of the financial health of each farm enterprise.

The 2024 Maryland enterprise budgets were developed using average yields and estimated input costs based on producer and farm supplier data. Fertilizer prices, pesticide availability, and fuel expenses have fluctuated greatly. The figures presented are averages and vary greatly from one farm and region to the other. It is, therefore, crucial to input actual farm data when completing enterprise budgets for your farm.

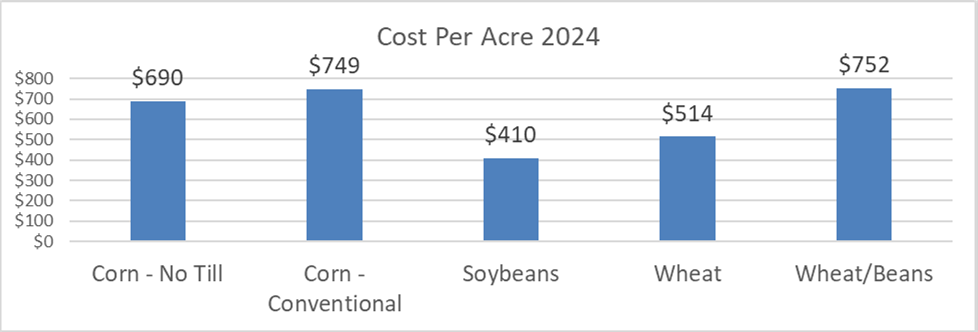

Cost Per Acre, 2024

Year

Corn

No Till

Corn

Conventional

Soybeans

Wheat

Wheat/Beans

2021

$540

$592

$346

$401

$608

2023

$736

$800

$423

$538

$800

2024

$690

$749

$410

$514

$752

Difference 23-24

-$46

-$51

-$13

-$24

-$48

Percent Change

-6%

-6%

-3%

-4%

-6%

How to Use University Enterprise Budgets

The enterprise budgets can be used as a baseline for your operation, and you can change these budgets to include your production techniques, inputs, and overall management. The budgets are available electronically in PDF or Excel. Use this document as a start or reference to create your crop budgets. Contact information is on the website if you have problems downloading any information.

2024 Crop Summary

Cost per acre expenses for 2024 have decreased a small amount from 2023 record highs. Based on estimates received cost of production includes: corn no-till costs $690 per acre, corn conventional $749 per acre, soybeans $410 per acre and wheat $514 per acre. While these are slightly (3-6%) lower than 2023 they are still 16%-22% higher than prices just 3 years ago (2021).

An Agricultural Technician is sought to provide technical support for the State Extension Agronomist with applied research and extension programming. This program performs applied research at seven UMD Research and Education Centers located across the state related to the production of corn, soybean, wheat, barley, and other crops of interest to Maryland producers. The incumbent may assist with research performed at private farms within Maryland. The incumbent will also assist with Extension programming, including preparation for field days, twilight tours, or other educational events.

To view the complete listing and to apply, go to https://ejobs.umd.edu/postings/117883. Best consideration date is April 4, 2023 and all applications must be submitted through the website. For questions or inquiries, contact Nicole Fiorellino at nfiorell@umd.edu.