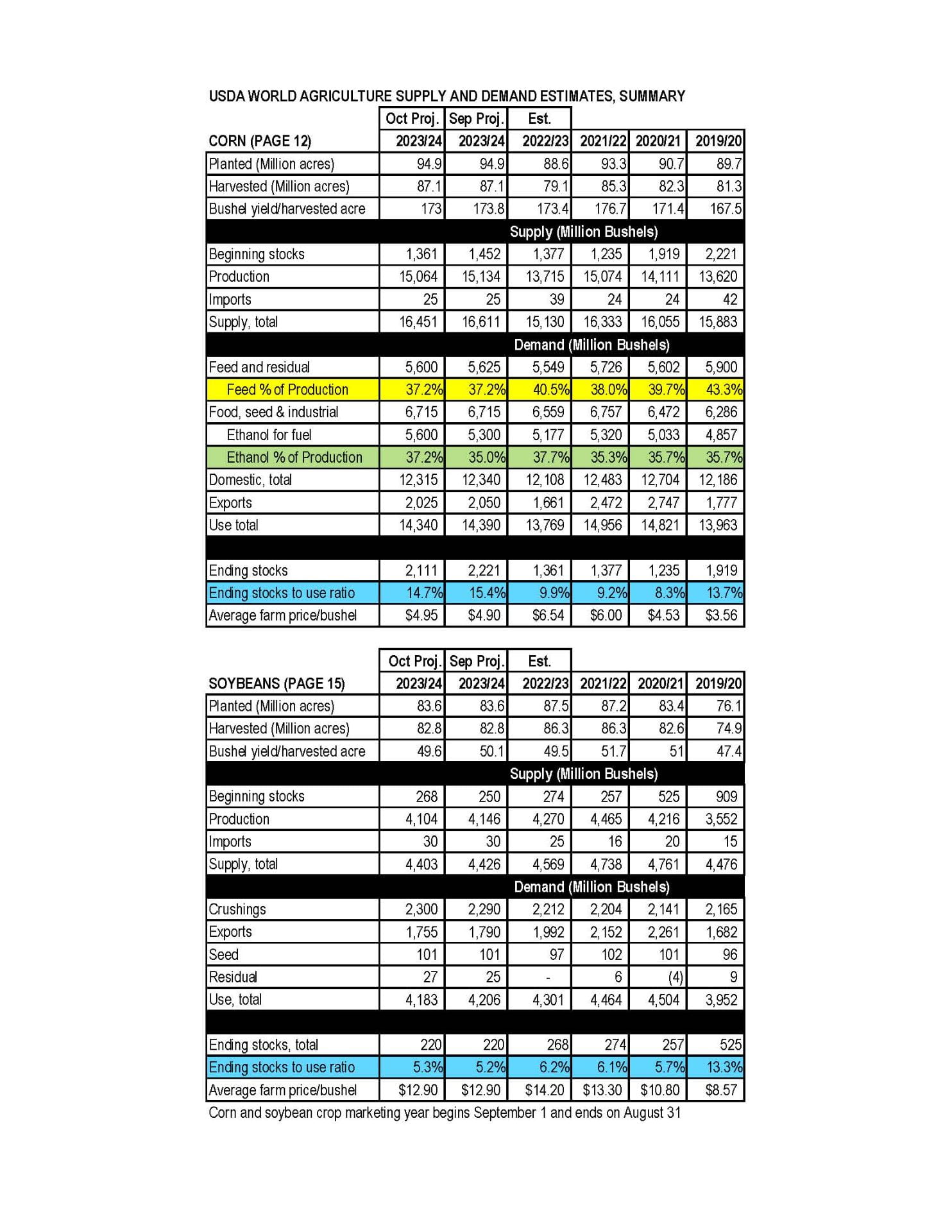

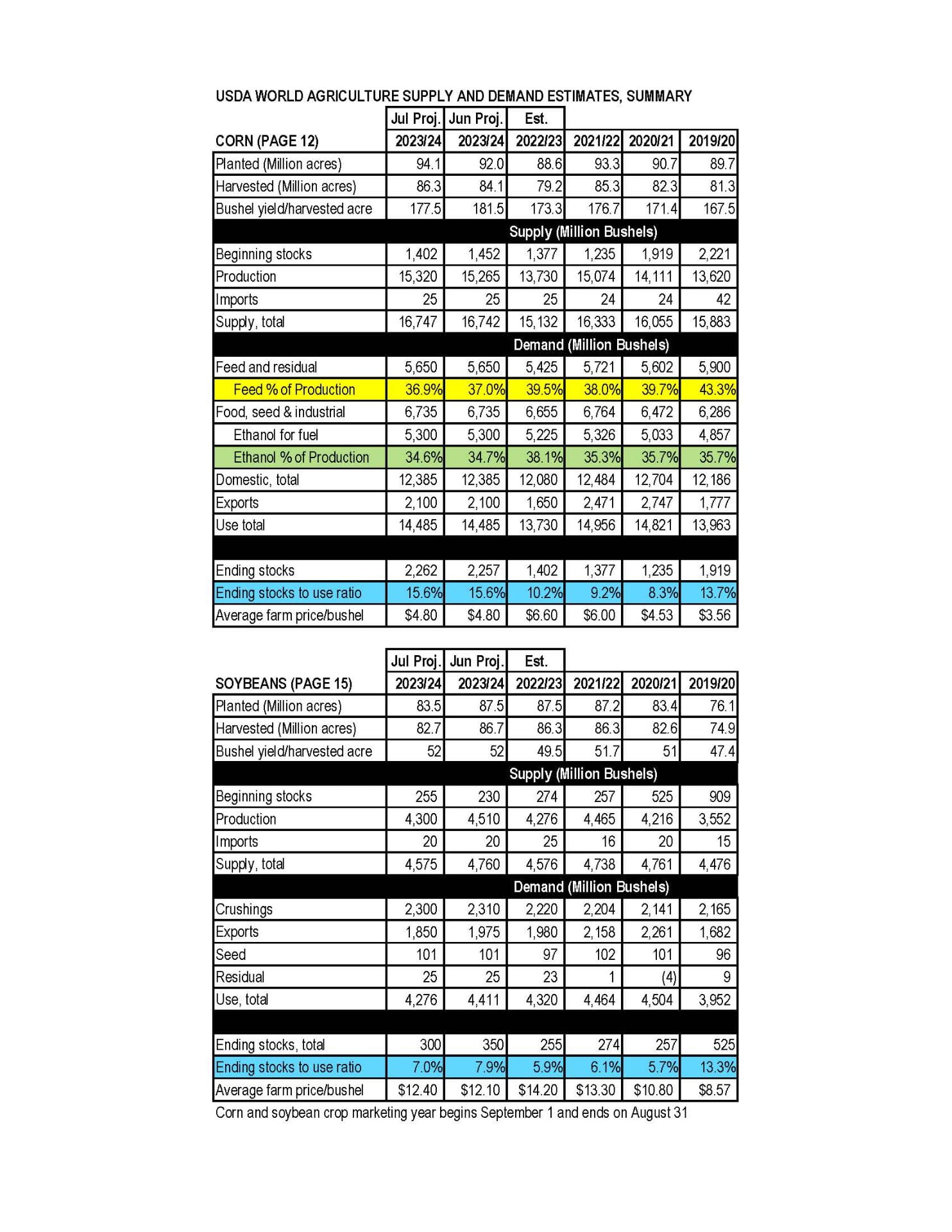

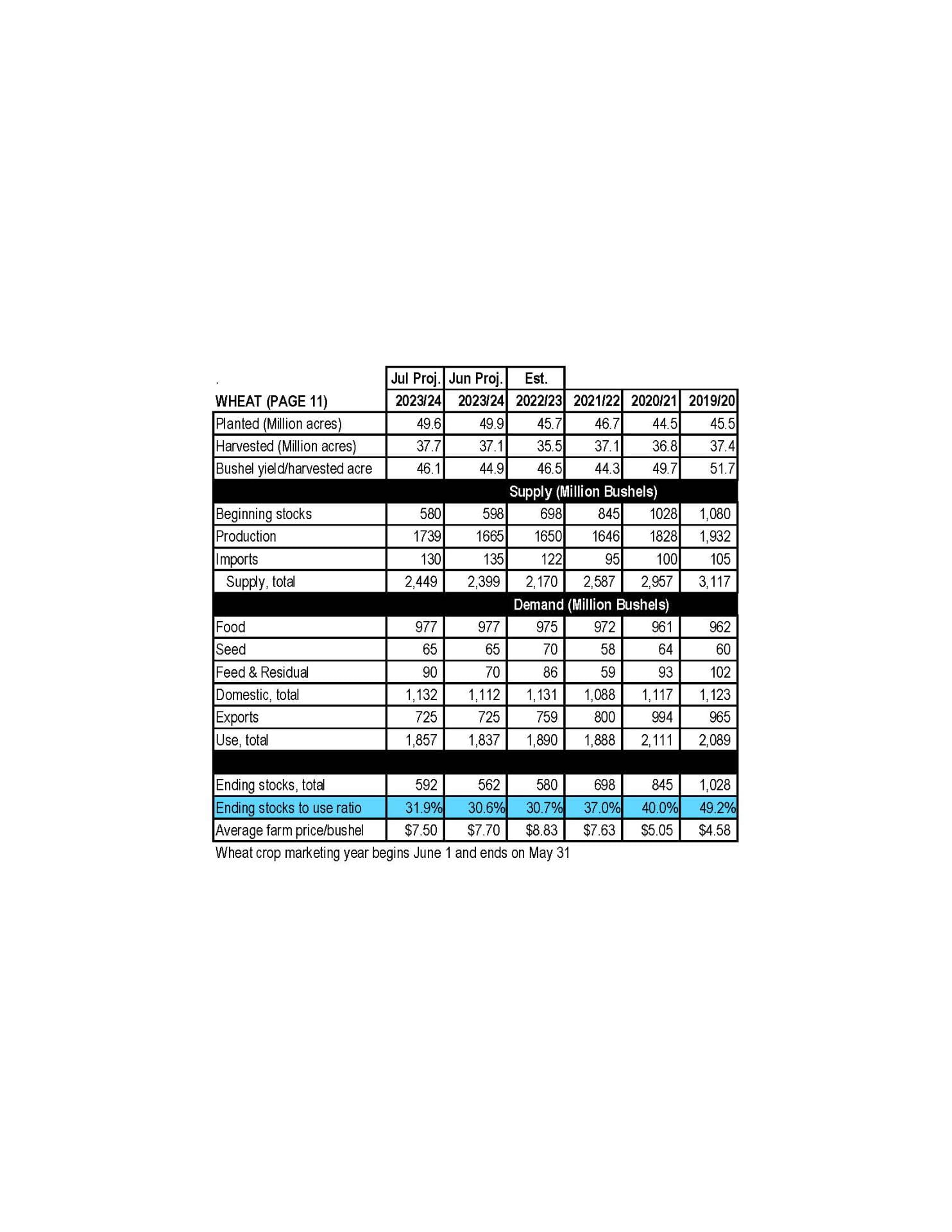

Attached is the summary for the October 2023 WASDE.

Corn

This month’s 2023/24 U.S. corn outlook is for reduced supplies, lower feed and residual use and exports, and smaller ending stocks. Corn production is forecast at 15.064 billion bushels, down 70 million on a cut in yield to 173.0 bushels per acre. Corn supplies are forecast at 16.451 billion bushels, a decline of 160 million bushels from last month, with lower production and beginning stocks. Exports are reduced by 25 million bushels reflecting smaller supplies and slow early-season demand. Feed and residual use is down 25 million bushels based on lower supply. With supply falling more than use, corn ending stocks for 2023/24 are lowered 110 million bushels. The season-average corn price received by producers is raised 5 cents to $4.95 per bushel.

Soybean

Soybean production is forecast at 4.1 billion bushels, down 42 million on lower yields. Harvested area is unchanged at 82.8 million acres. The soybean yield is projected at 49.6 bushels per acre, down 0.5 bushels from the September forecast. The largest production changes are for Kansas, Michigan, and Nebraska. With lower production partly offset by higher beginning stocks, supplies are reduced 24 million bushels. Soybean exports are reduced 35 million bushels to 1.76 billion with increased competition from South America. Soybean crush is projected at 2.3 billion bushels, up 10 million, driven by higher soybean meal exports and soybean oil domestic demand. Soybean oil domestic use is raised in line with an increase for 2022/23. With lower exports partly offset by increased crush, ending stocks are unchanged from last month at 220 million bushels.

Wheat

The outlook for 2023/24 U.S. wheat this month is for higher supplies, increased domestic use, unchanged exports, and higher ending stocks. Supplies are raised 85 million bushels, primarily on higher production as reported in the NASS Small Grains Annual Summary, released September 29. Domestic use is raised 30 million bushels, all on higher feed and residual use. The NASS Grain Stocks report released September 29 indicated a higher year-to-year increase for first quarter (June-August) domestic disappearance than previously expected. Exports remain at 700 million bushels with several offsetting by-class changes. Projected ending stocks are raised by 55 million bushels to 670 million, up 15 percent from last year. The season average farm price is reduced $0.20 per bushel to $7.30 on higher projected stocks and expectations for futures and cash prices for the remainder of the marketing year.

Kelly Hamby, Associate Professor and Extension Specialist, University of Maryland and

David Owens, Extension Entomologist, University of Delaware

Figure 1. Barley Yellow Dwarf patch in a field of malting barley, March 2023. Photo: David Owens, Univ. of Delaware.

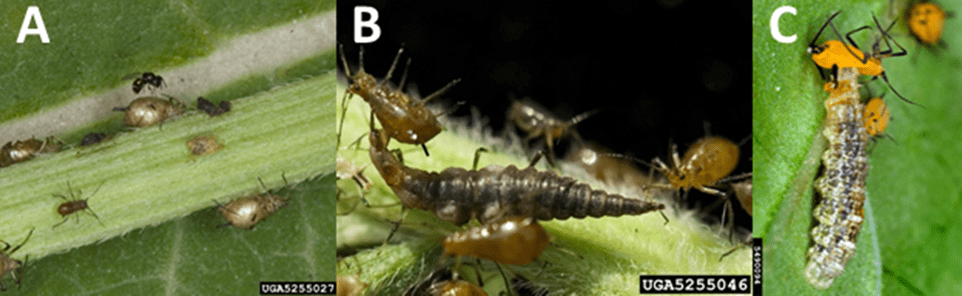

Last season, aphids transmitted an unusual amount of barley yellow dwarf virus (BYDV) to wheat and barley across the Delmarva Peninsula. BYDV is particularly important when it infects plants in the fall. Fall BYDV infections can stunt plants (noticed as early as green-up, Figure 1) and cause more serious yield loss than spring infections. Our most common small grain aphid species are bird cherry oat aphid (Figure 2) and English grain aphid, although bird cherry oat aphid are associated with greater and more severe incidence of BYDV.

Figure 2. Bird cherry-oat aphids.

Historically, planting after the Hessian fly-free date (Table 1) reduced the likelihood of fall BYDV infection. However, fly-free dates were calculated more than 100 years ago, and it is now not uncommon for our first killing frosts to occur in late October or even November. Long falls with milder weather allow more time for aphids to colonize fields and potentially transmit the virus. Small grains varieties vary in their susceptibility to BYDV, and planting varieties with at least some tolerance can help. Unfortunately, resistant varieties are not available in barley. Finally, monitoring and managing the aphid vectors may be necessary.

Identifying bird cherry-oat aphid: A magnifying hand lens is required to identify aphids. Bird cherry-oat aphid ranges from orange green to olive green to greenish black. Wingless individuals typically have a reddish orange patch around the base of the cornicles (tail pipes). Winged individuals tend to be very dark. Their legs, cornicles, and antennae are similar in color to their bodies and medium in size.

Monitoring and thresholds: Typically, monitoring aphids in the fall and at green-up provides the best chance of identifying and mitigating BYDV risk. Scout ten locations per field avoiding field margins and look at 1 ft of row in each, making sure to look at the crown (at or below ground level), at the stem, and on the undersides of leaves. English grain aphids tend to feed on the uppermost portions of the plants while bird cherry oat aphids tend to cluster on the lower portions, especially in barley.

University extension threshold recommendations vary by region. In southern states, 6 aphids/row-ft is considered justification for a treatment in the fall. North Carolina uses a threshold of 20 aphids/row-ft where BYDV has been a problem and cold weather is not in the 7 day forecast. For other small grains, consider increasing the threshold to 25-50 aphids per foot of row.

In 2022, one of the malting barley fields sampled averaged 17 aphids per row-ft in early November. Because of unusually warm winter weather in which average temperatures were greater than 38 degrees, aphid populations peaked in one field at 235 aphids per row-ft that had averaged 1.8 per row-ft in November. This highlights the need to regularly monitor aphid populations during periods of mild weather.

Natural enemies: A number of natural enemies feed upon or parasitize aphids and they often do a good job keeping aphid populations down. One natural enemy per 50-100 aphids should be sufficient to control aphid populations. In addition, they are good at finding aphids even when their populations are low. Small wasps that develop within aphids leaving behind “mummy” aphids (Figure 3A), lady beetles, lacewing larvae (Figure 3B), and flower fly larvae (Figure 3C) are especially common aphid natural enemies. Insecticides will also kill these natural enemies.

Figure 3. Aphid natural enemies A) parasitoid wasp and golden or tan colored “mummy” aphids, B) lacewing larva eating aphids, C) flower fly larva eating aphids. Images: David Cappaert, Bugwood.org.

Insecticides: Seed treatments (e.g., Cruiser, Gaucho) provide some protection from fall aphids, but do not continue to provide protection into the spring and are not economic in years where aphids do not occur. Due to the differences in economics and BYDV susceptibility of malting barley varieties, seed treatments may be more useful than in feed barley or wheat. We generally recommend a foliar insecticide when aphid populations reach threshold. Small grain aphids are generally quite susceptible to insecticides. Pyrethroid products (e.g., Warrior) or a pyrethroid-neonicotinoid mix (e.g., Endigo, labeled for barley only) work well for aphid control.

Table 1. Hessian fly-free dates for Maryland and Delaware counties

Flanders, K., Herbert, A., Buntin, D., Johnson, D., Bowen, K., Murphy, J. F., Chapin, J., Hagan, A. 2006. Barley Yellow Dwarf in Small Grains in the Southeast. https://entomology.ca.uky.edu/files/efpdf1/ef150.pdf.

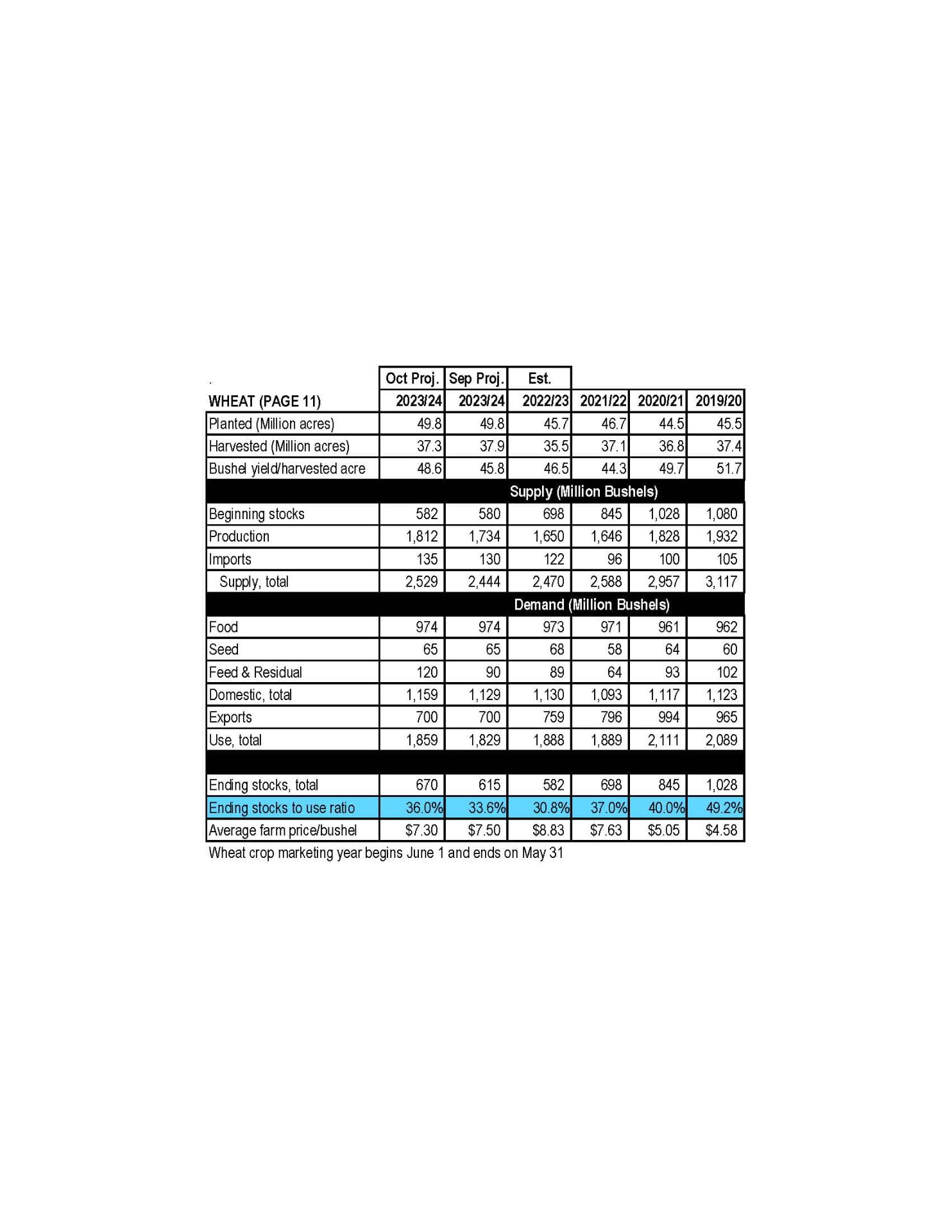

Attached is the summary for the September 2023 WASDE.

Corn

This month’s 2023/24 U.S. corn outlook is for slightly larger supplies and ending stocks. Projected beginning stocks for 2023/24 are 5 million bushels lower based on mostly offsetting trade and corn used for ethanol changes for 2022/23. Corn production for 2023/24 is forecast at 15.1 billion bushels, up 23 million from last month as greater harvested area more than offsets a reduction in yield. The national average yield is forecast at 173.8 bushels per acre, down 1.3 bushels. Harvested area for grain is forecast at 87.1 million acres, up 0.8 million. Total U.S. corn use is unchanged at 14.4 billion. With supply rising slightly and use unchanged, ending stocks are up 19 million bushels to 2.2 billion. The season-average corn price received by producers is unchanged at $4.90 per bushel.

Soybeans

U.S. soybean supply and use changes for 2023/24 include lower beginning stocks, production, crush, exports, and ending stocks. Lower beginning stocks reflect an increase for exports in 2022/23. Soybean production is projected at 4.1 billion bushels, down 59 million with higher harvested area offset by a lower yield. Harvested area is raised 0.1 million acres from the August forecast. The soybean yield of 50.1 bushels per acre is down 0.8 bushels from last month. The soybean crush forecast is reduced 10 million bushels and the export forecast is reduced 35 million bushels on lower supplies. Ending stocks are projected at 220 million bushels, down 25 million from last month. The U.S. season-average soybean price is forecast at $12.90 per bushel, up $0.20 from last month. The soybean meal price is unchanged at $380 per short ton and the soybean oil price is raised 1.0 cent to 63.0 cents per pound. Other changes this month include higher peanut and lower cottonseed production.

Wheat

The 2023/24 U.S. all wheat outlook for supply and use is unchanged this month with offsetting by-class changes on exports. The projected 2023/24 season-average farm price is also unchanged at $7.50 per bushel.

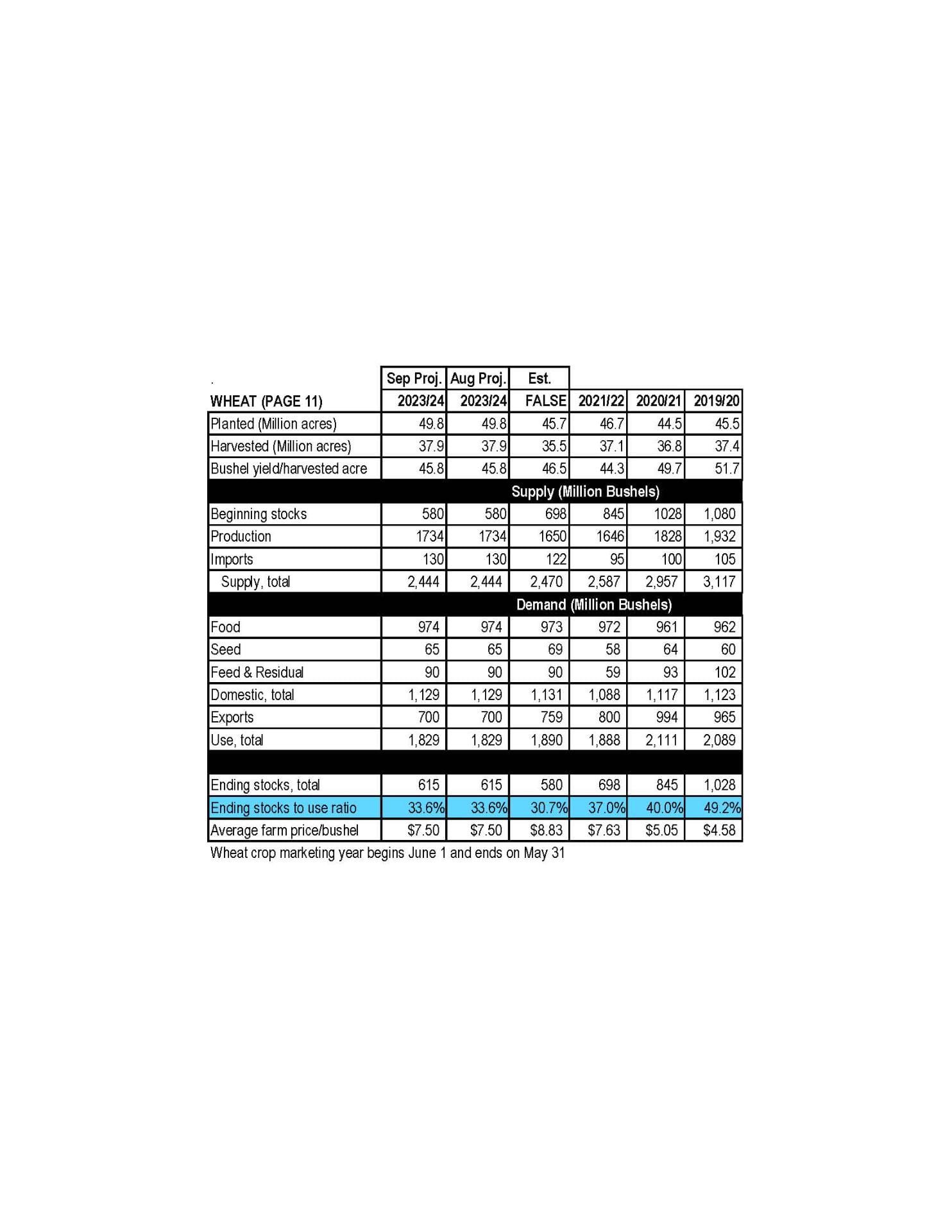

This month’s 2023/24 U.S. corn outlook is for fractionally higher supplies and ending stocks. Corn beginning stocks are lowered 50 million bushels, as greater feed and residual use for 2022/23 more than offsets reductions in corn used for ethanol and exports. Corn production for 2023/24 is forecast up 55 million bushels as greater planted and harvested area from the June 30 Acreage report is partially offset by a 4.0-bushel reduction in yield to 177.5 bushels per acre. According to data from the National Centers for Environmental Information, harvested-area-weighted June precipitation data for the major Corn Belt states represented an extreme downward deviation from average. However, timely rainfall and cooler than normal temperatures for some of the driest parts of the Corn Belt during early July is expected to moderate the impact of June weather. For much of the crop the critical pollination period will be in the coming weeks. With supply rising fractionally and use unchanged, ending stocks are up 5 million bushels. The season-average farm price received by producers is unchanged at $4.80 per bushel.

Soybean

Soybean production is projected at 4.3 billion bushels, down 210 million on lower harvested area. Harvested area, forecast at 83.5 million acres in the June 30 Acreage report, is down 4.0 million from last month. The soybean yield forecast is unchanged at 52.0 bushels per acre. With lower production partly offset by higher beginning stocks, 2023/24 soybean supplies are reduced 185 million bushels. Soybean crush is reduced 10 million bushels reflecting a lower soybean meal domestic disappearance forecast. Soybean exports are reduced 125 million bushels to 1.85 billion on lower U.S. supplies and lower global imports. With lower supplies only partly offset by reduced use, ending stocks for 2023/24 are projected at 300 million bushels, down 50 million from last month. The U.S. season-average soybean price for 2023/24 is forecast at $12.40 per bushel, up $0.30 from last month.

Wheat

Changes this month to the 2023/24 U.S. wheat outlook increase supplies and domestic use, leave exports unchanged, and increase ending stocks. Supplies are raised on larger production, which is up 74 million bushels to 1,739 million, on higher harvested area and yields. The first 2023/24 survey-based production forecast for other spring and Durum indicates a decrease from last year. Conversely, winter wheat production is forecast higher on larger harvested area and higher yields. Gains for all wheat production are partly offset by smaller beginning stocks, which are lowered 18 million bushels to 580 million as indicated in the Grain Stocks report, issued June 30. The 2023/24 ending stocks are forecast at 592 million bushels, 30 million higher than last month. The projected season-average farm price is forecast at $7.50 per bushel, down $0.20 from last month.

Nathaniel Bruce, Farm Business Specialist, University of Delaware and Mark Townsend, Agriculture Agent Associate, University of Maryland Extension, Frederick County

June proved volatile for grain markets. To recap, the December 2023 contract rallied off its $4.90 lows from late-May, peaking at $6.29 on June 21st and has precipitously fallen back below $5.00 at the time of writing this article. As it does, the soft red winter wheat market followed suit in the September contract with a big swing from the $5.87 lows on June 1st to a high on June 26th at $7.70 only to plummet back to earth reaching $6.51 currently. No less, the November soybean market followed a similar pattern rising from $11.30 on June 1st to peaking at $13.77 on June 21st, and then tumbling back some in the last week of June only to find levity on the last day of the month.

It’s not difficult to convey the gravity of these swings: In one singular month, we saw a $1.39 gain and decline in the corn market, a $1.87 upswing and $1.19 downfall in the wheat market, and a $2.07 upswing with a $1.13 retracement followed by an $0.76 movement higher on the last trading day of the month in the soybean market.

The summary begs the questions: how can we explain the volatility of these markets and what can we do as producers to limit our risk to any further price loss?

Firstly, the phenomena we have encountered this last month can be described as the result of a “weather market”—a period of time in which traders make decisions based on current and prospective weather conditions that affect the production (supply) of a particular commodity in hopes of capturing a premium related to production risk. Put another way, this is a “supply-side” market driver as there is a risk to the volume of production.

The weather in question is that of the central United States as the region is under varying degrees of drought. The most recent USDA Drought Monitor (6/29/2023) report indicates that 53% of the contiguous United States is experiencing some level of drought. On a per crop basis the monitor indicates that 70% of corn growing regions and 63% of soybean growing regions are in some degree of drought. Reports in June indicated progressively higher levels of moisture stress in large swaths of the corn belt. As we well know, corn demands roughly an inch of rain each week when in the rapid growth stages and entering pollination. With this, traders bet on a reduction in yield for this year’s corn crop, thus raising the price through market actions.

Traders not only looked at retrospective reports like the drought monitor, but also analyzed weather forecasts for these regions. For much of the month, neither the GFS (U.S. based) nor the ECMWF (European based) weather models predicted any significant rainfall for these regions. In some instances, the models added further uncertainty as the GFS forecasted sporadic precipitation events while the ECMWF left the radar screen blank. On the ground, drought regions experienced high winds and high temperatures further drying out soils and inducing greater rates of transpiration from an already moisture-stressed crop.

With these factors at play, market participants found reason to purchase grain futures contracts or options in hopes of realizing some future increases in commodity prices. The Commodity Futures Trading Commission (CFTC) reports the commitment of traders market positions in which the non-commercial speculative entities (aka “the funds”–referring to money managers like hedge funds or mutual funds) with significant market power were in a net short position by about 60-70k contracts of corn entering the month of June. As the month progressed, the most recent report indicates that these market participants held a 100-115k net long position (As of 6/27/2023). Effectively, this means that these market participants were betting on a decline in the corn futures market at the end of May, only to quickly reverse course and bet a far larger position on an increase in the corn futures market price. There is a significant delay in the release of these reports, so it is difficult to ascertain where the funds stand after the last week in June ending in a Friday sell-off in corn and wheat. Though current estimates place fund positions back to near neutral (equal quantity of long and short positions) in corn. Traders in the wheat futures market followed a similar path to corn, while traders in the soybean futures market are currently estimated to be in a significantly long position.

The weather trading continued later into the month; price action in the last week of June saw falling prices as regions of the Midwest realized modest precipitation accumulations. No less, the GFS and ECMWF weather models agreed on additional future precipitation events thus indicating a potential for salvage of the current crop.

To cap off an already topsy-turvy last week in June and generally volatile month, the USDA released Quarterly Grain Stocks and Planted Acreage reports on Friday, June 30th. The grain stocks report followed analysts estimates, however the planted acreage report unexpectedly and significantly deviated from the market sentiments. Reported planted corn acreage rose roughly 2 million acres from a previous prediction report, and an increase of about 5% from last year. Soybean acreage fell by about 5% compared to last year, which is about 4.2 million acres lower than the average trade estimate. Markets traded this supply-side news as corn fell back to prices not seen since December of 2020. On the other hand, the soybean market is trading back to levels from mid-June.

The volatility of these markets is unmistakably high. Not only is the current implied volatility of these markets (based on options prices) higher than 60-80% of all trading days in the previous year, but trading strategies involving options require larger investments.

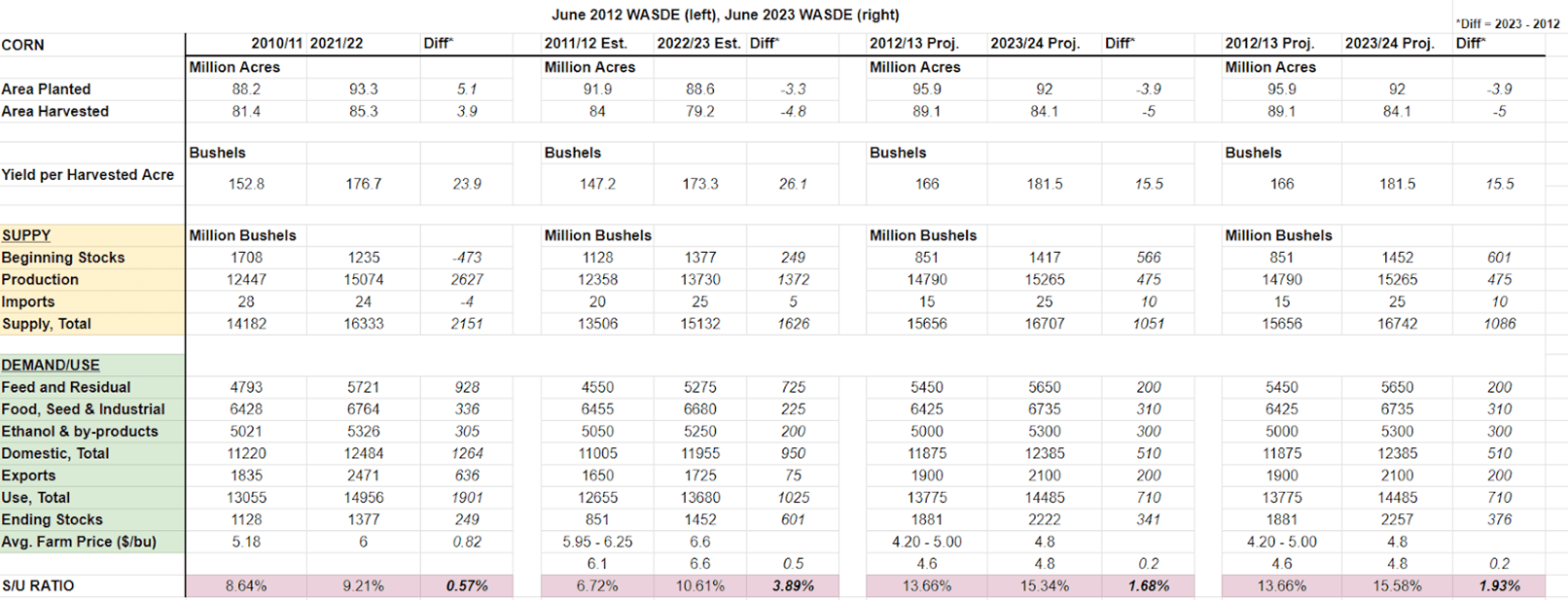

Figure 1. Corn 2012 vs 2023.

Marketing a crop in these conditions is undoubtedly challenging. We may look to previous years for guidance, though even this is uncertain. Analysts have likened the run-up in the grain markets to those in 2012 when a similar drought induced crop failures across the Midwest. Currently, there exists a 0.56 correlation coefficient between the 2012 December contract and the 2023 December contract (Figure 1). In truth, this exact discussion is nothing new; many marketing professionals and memorious farmers recall the drought of 2012 that spurred a dramatic run-up in the corn price reaching a peak of $8.49 on August 10th, 2012 and will refer to this observation whenever a drought emerges in the Midwest. Although, there is a correlation in prices between Dec’12 Corn and Dec’23 corn, the fundamental supply and demand picture is vastly different between 2012 and 2023 as there is nearly 4% larger Stocks-to-Use ratio in 2023 than 2012 given the current lack-luster export, feed, and ethanol demand we have experienced for the current marketing year.

Figure 2. USDA WASDE June 2012 vs. June 2023.

Other more bearish investors have noted that the current price trend is more similar to 1992 in which an early season drought induced volatility and rising prices. Contrary to 2012, the 1992 corn market saw a dramatic price decline after timely and significant rains busted the drought and produced a near trend-line crop yield.

So how does one effectively market a crop this year? The first step as always is to know the cost of production taking into actual input price figures to uncover an operation’s breakeven price and yield. Yield does play a critical role in determining these figures, though as we know yield is not the sole driver of profitability. Please refer to the University of Maryland Extension website for enterprise budget templates here: https://extension.umd.edu/programs/agriculture-food-systems/program-areas/farm-and-agribusiness-management/grain-marketing.

Certainly a next step would be to look for ways to offset future price risk. Depending on the level of familiarity, options strategies could offer additional downside protection. However, this is most commonly accomplished by forward contracting some of the new crop. At the time of writing, the soybean market continues to rise modestly above estimated cost of production figures for Central Maryland. Producers may find these prices profitable and would be well advised to limit potential downside risk.

Marketing professionals offer that producers may find shelter in short-run run-ups to sell new crop corn and stored wheat. Some analysts predict that the USDA may have to revise yield estimates lower given the potential damage done to the corn crop of the Midwest. The market may react to this revision lower, whereby the watchful marketer could capitalize on a small upward price movement. Yes it is tempting to wait for the next larger rally in the market, but waiting to find the top of the curve may prove far more risky than taking smaller profits. A wise farmer once said that he stayed in business for many years because, “I always took my profits too early.”

Nicole Fiorellino, Extension Agronomist | nfiorell@umd.edu University of Maryland, College Park

Figure 1. Extreme example of pre-harvest sprout in wheat. Image: Ohio State University.

2023 was shaping up to be a decent wheat season, with mild winter and minimal disease impacts this spring. Although some areas of the state were dry, there were some timely rains at the end of April to get the crop through the rest of the season. We sometimes forget that wheat thrives in much drier climates than the Northeast, and what seems dry to us was probably ideal for wheat.

As wheat harvest is currently underway in some areas of the state, the hopes of high yields and disease-free grain may now be riddled with an unseen quality blemish – falling falling numbers. Growers producing wheat for use in milling or baking are paying attention to quality measures such as falling numbers, or the activity of the alpha amylase enzyme in the grain stemming from pre-harvest sprouting. As grain begins sprouting within the head, prior to harvest, alpha amylase builds up and degrades starch, which decreases flour quality. To measure falling numbers, a slurry of grain meal and water is mixed and a plunger is dropped into the slurry, with the time measured for the plunger to drop through the slurry. High alpha amylase results in low starch, which thins the slurry and the plunger falls quicker, resulting in lower falling number measures. In short, low falling numbers equals bad quality wheat that is not suitable for milling or baking.

Causes of low falling numbers, similar to disease pressure, are somewhat out of a grower’s control and not very well understood. Some areas of the state received a respite from the dry conditions, in the form of a few days with a small amount of precipitation towards the end of June. While our corn crop happily received the moisture, this was enough rain in some areas to not only delay the beginning of wheat harvest but signal the wheat grain to break dormancy and begin to sprout. Low falling numbers may also be observed in grain that did not sprout due to a defect known as late maturity alpha amylase (LMA). This is the buildup of alpha amylase in the wheat grain triggered by cold stress during maturation. It is still unclear how to specifically define “cold stress” that causes LMA but it is yet another process that increases alpha amylase in the wheat grain, decreasing flour quality. In any given season, low falling numbers can be a result of either pre-harvest sprouting or LMA or even both conditions. Susceptibility to pre-harvest sprouting and LMA are genetically linked, but even with genetic resistance, the interaction between genetics and environmental conditions can still result in decreased falling numbers.

For the 2023 wheat crop, it is important to get wheat harvested as soon as possible. There is no way to correct for falling numbers now, but growers can make every effort to get wheat out of the field as quickly as possible to avoid exposure to additional precipitation events. While all hope is not lost and wheat with low quality can still be sold for feed, any potential premiums for producing high quality wheat will be lost. For future seasons, Maryland growers can make an effort to select early maturing wheat varieties, to hopefully expedite harvest in the spring. We know the down-season benefits of early wheat harvest, such as earlier planting and higher yields of double crop soybeans, and we are also aware of the potential risk of frost damage to early maturing wheat. However, early maturing wheat varieties may be a the best option to mitigate quality issues. While your premium for 2023 may be lost, you should begin discussing your 2024 wheat crop with your crop insurance agent now, especially if you are planning to grow high quality wheat for milling or baking. There may be coverage options available to protect you from lost premiums due to poor falling numbers, for example, so now is the time to plan accordingly for 2024.

Reports are for crop conditions up to June 1, 2023.

Western Maryland

To say we are dry would be an understatement. Corn planting is winding down and the last of the full-season beans will soon be finished up too. Barley and wheat are in full head a bit ahead of normal, whatever that is. The dry weather is a good thing for cereals as the conditions are poor for fungal growth. It will be interesting to see what effect the dry weather will have on test weight and yield. First cutting alfalfa and most of the grass hay is in the barn or silo. Rain will be important very soon for forage regrowth and corn and bean growth. The cool evenings and overnights have been the only blessing but heat is on the way.—Jeff Semler, Washington Co.

Central Maryland

Frederick County has finished planting corn. There may be the occasional field that remains, but this is the exception. Early corn is at the V4-5 stage while later planted fields are approaching V2. Seedling diseases have been nearly non-existent in scouted fields, though wireworm pressure has been observed in both corn and soybean fields. Soybeans are 90% planted; early beans are around V2 while most are VC-V1. The majority of the hay crop is made and in the barn. Annual weeds have emerged and are approaching a foot tall in some fields, though weed pressure has remained limited given the dry weather and resulting effective burndown applications. Second cutting alfalfa is underway, some weevil pressure had been observed in the occasional field though generally there has been relatively limited pressure. Most barley is at or near soft-dough stage, while the wheat crop has finished flowering and is moving into grain fill. Both small grain crops appear in good to great condition given the limited disease pressure.—Mark Townsend, Frederick Co.

Northern Maryland

We got through the entire month of May without any measurable precipitation. Such weather has made for great conditions for making hay, and this is one of the few times in recent memory where pretty much all of the first cutting hay crop was put up before June 1; although yields did appear to suffer in some fields due to the dry weather. 99% of the corn crop is planted and emerged, with earliest planted corn around V5-6. Almost all full-season soybeans have been planted and are anywhere from just planted to V3-4. Both corn and soybeans have yet to show wilting, but they are both growing very slowly due to the lack of rain. Fortunately we are running well below with temperatures in the 70s most of the month. Wheat is just starting to turn and appears to have very little disease pressure; we will see how the dry spring affects yield and test weight. We are hoping for a bit of rain in the coming weeks.—Andy Kness, Harford Co.

Upper and Mid Shore

Early planted corn greened up, but definitely has reduced yield potential. Later planted corn looks great- good color and uniform. Early beans are finally outgrowing slug feeding. Like corn, later beans look great. Barley harvest will begin 1st week of June. Wheat is starting to turn. There was great hay made last week. Soil conditions across the region are getting dry.—Jim Lewis, Caroline Co.

Lower Shore

Wheat and barley are drying down. Corn has been planted, and is generally around V1 to V5 stage. Most soybean has been planted and early soybean plantings have emerged. Herbicide-resistant weeds, such as common ragweed, marestail, and palmer amaranth, are starting to emerge. Scout and spray early to stay ahead on control. Some farmers have utilized late-terminated cover crops to help manage weed pressure through providing a mulch on the soil surface. Deer are prevalent in fields and causing damage on corn and soybean seedlings.—Sarah Hirsh, Somerset Co.

Southern Maryland

Temperatures finally touched the 80°F mark this week. Cooler temperatures and lack of rainfall has slowed crop progress in May. Most corn fields are a kaleidoscope of yellow shades and uneven stands. Black cutworms, slugs, wireworms and seed corn maggot are active across the region. We received scattered showers last weekend that helped crop conditions improve in most areas. Soybeans follow much of the same story. Early planted beans look decent. Barley is drying down with harvest expected any day. Wheat will not be far behind. Ryegrass continues to be a challenge for producers in both burndown situations in corn and beans, as well as small grains. My thought is the cooler weather is affecting the performance of glyphosate, especially on larger plants. The pockets of glyphosate resistant ryegrass are expanding in our area as well. The drier weather has been good for making hay- we saw a lot of balers in the field last week.—Ben Beale, St. Mary’s Co.

The program will start at the seed building and proceed to the fields. We will hear an update on the Agronomy degree program within the Department of Plant Science and Landscape Architecture, including highlights from the first semester teaching AGST401: Tractor and Equipment Operation, Safety and Maintenance. We will showcase a commercial variety strip trial organized by the Maryland Crop Improvement Association (MCIA) and industry reps will be on hand to discuss their entries in the trials. Dr. Vijay Tiwari will discuss the small grain variety trials and his wheat breeding program, Dr. Nidhi Rawat will discuss her pathology work in barley and wheat, and Dr. Kurt Vollmer will update us on weed control in wheat.

Dinner will be served at 5pm, sponsored by Maryland Crop Improvement Association and others.For additional program information, contact Dr. Nicole Fiorellino at nfiorell@umd.edu or 443-446-4275.

Information from USDA WASDE report

Information from USDA WASDE report