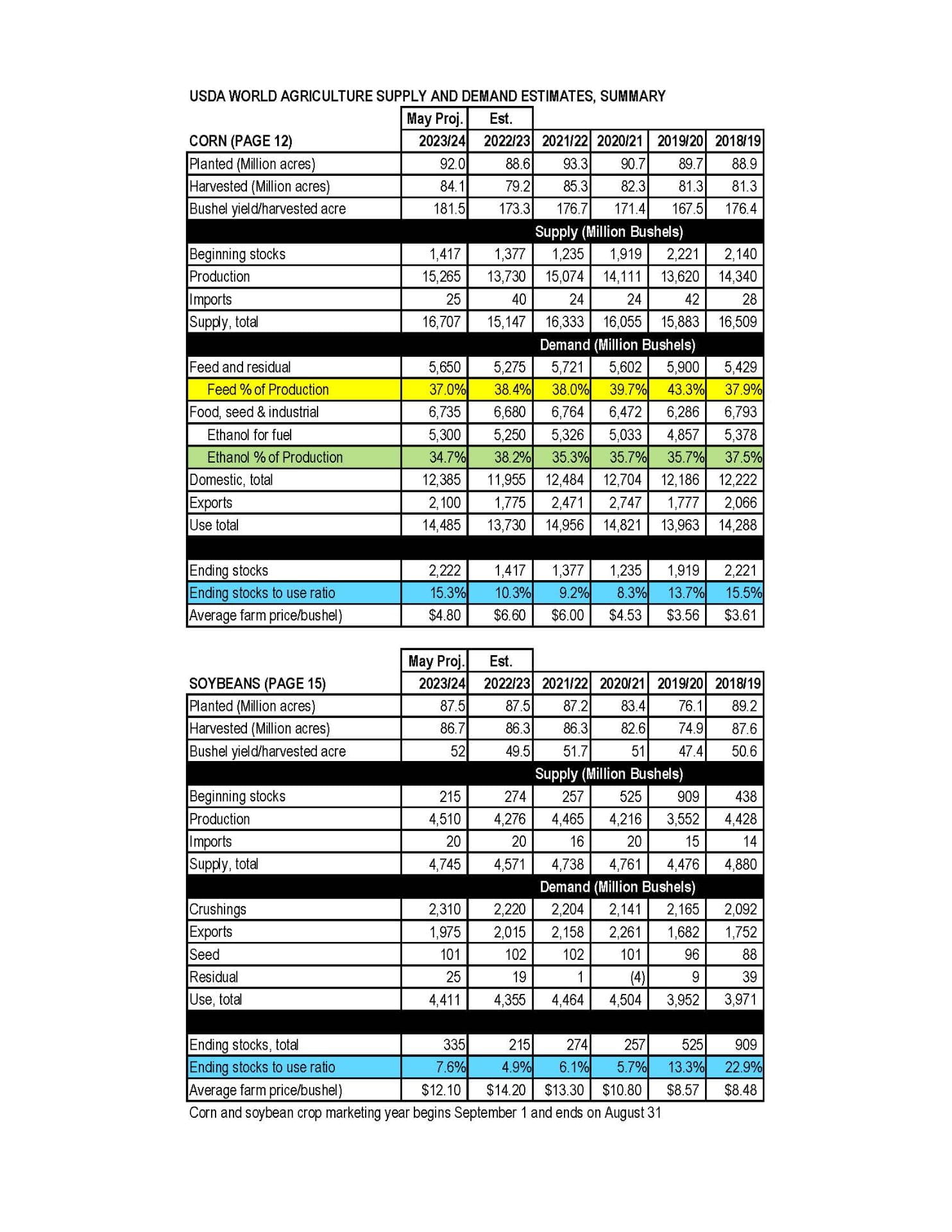

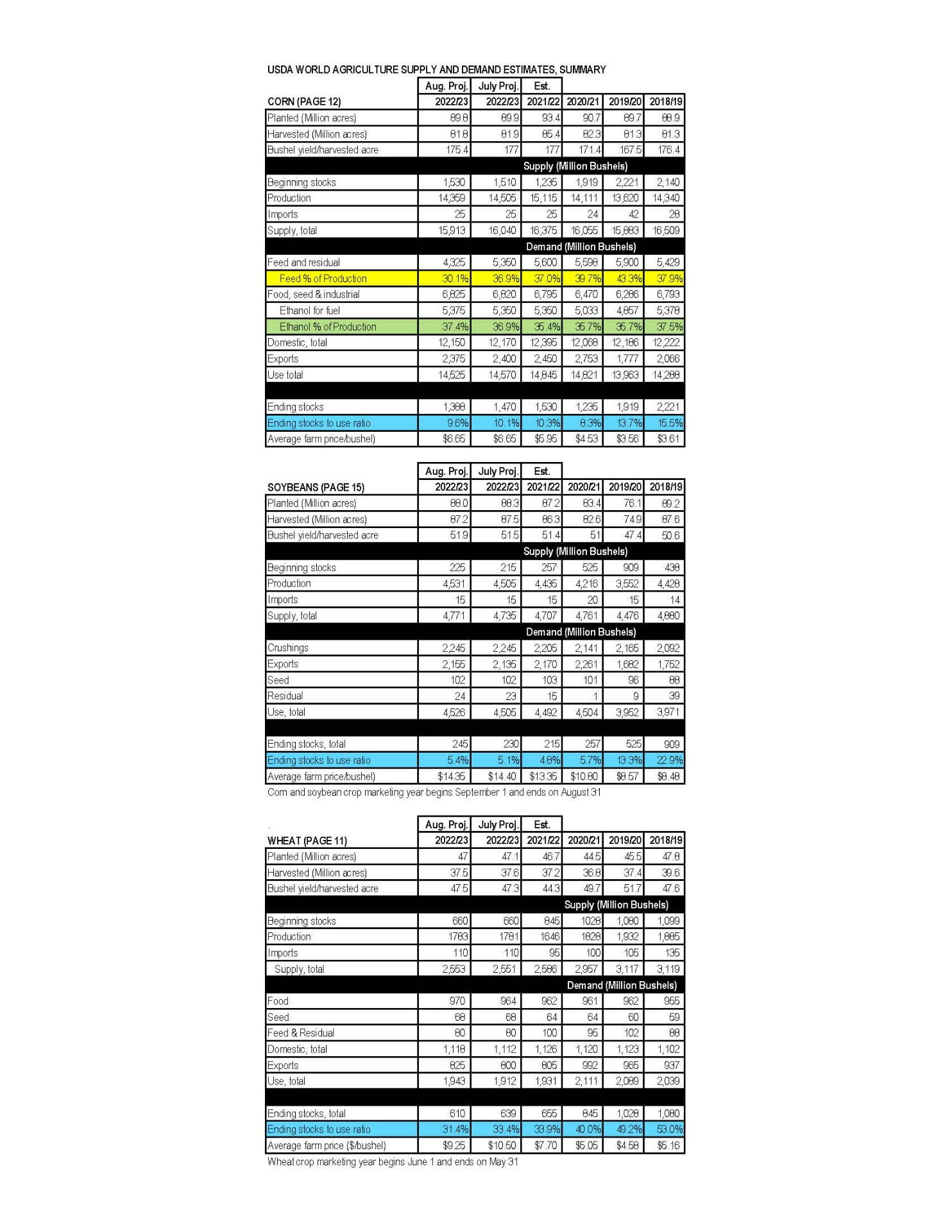

The 2023/24 U.S. corn outlook is for larger production, greater domestic use and exports, and higher ending stocks. The corn crop is projected at a record 15.3 billion bushels, up more than 10 percent from last year on increases to both area and yield. The yield projection of 181.5 bushels per acre is based on a weather-adjusted trend assuming normal planting progress and summer growing season weather, estimated using the 1988-2022 time period. With beginning stocks up slightly, total corn supplies are forecast at 16.7 billion bushels, the highest since 2017/18. Total U.S. corn use for 2023/24 is forecast to rise about 5 percent relative to a year ago on higher domestic use and exports. Food, seed, and industrial use is projected to rise 55 million bushels to 6.7 billion. Corn used for ethanol is projected to increase 1 percent, based on expectations of modest growth in motor gasoline consumption and ethanol’s inclusion rate into gasoline. Feed and residual use is projected higher on a larger crop and lower expected prices. U.S. corn exports for 2023/24 are forecast to rise 325 million bushels to 2.1 billion, as lower prices support a sharp increase in global trade following the decline seen during 2022/23. U.S. market share is expected to increase slightly albeit remain below the average of the past 5 years. Exports are higher for Argentina and Brazil, with the former reflecting a return to normal weather conditions after a drought during 2022/23. Despite a rebound in U.S. exports, Brazil is forecast to be the world’s largest exporter of corn for the second consecutive year. Exports for Ukraine are projected to decline based on lower production prospects. With total U.S. corn supply rising more than use, 2023/24 ending stocks are up 805 million bushels from last year and if realized would be the highest in absolute terms since 2016/17. Stocks would represent 15.3 percent of use, the highest since 2018/19. The season-average farm price is projected at $4.80 per bushel, down $1.80 from 2022/23.

Soybean

The 2023/24 outlook for U.S. soybeans is for higher supplies, crush, and ending stocks, and lower exports compared with 2022/23. The soybean crop is projected at 4.51 billion bushels, up 5 percent from last year’s crop mainly on higher yields. With lower beginning stocks partly offsetting increased production, soybean supplies are forecast at 4.75 billion bushels, up 4 percent from 2022/23. Total U.S. oilseed production for 2023/24 is projected at 132.8 million tons, up 6.9 million from 2022/23 mainly on higher soybean production. Production forecasts are also higher for canola, peanuts, and cottonseed. The U.S. soybean crush for 2023/24 is projected at 2.31 billion bushels, up 90 million from the 2022/23 forecast on favorable crush margins and strong demand for soybean oil as a biofuel feedstock, which is projected to increase 900 million pounds to 12.5 billion. Domestic soybean meal disappearance is forecast to increase 2 percent from 2022/23 on lower soybean meal prices and modest growth primarily in poultry production. U.S. soybean meal exports are forecast at 14.8 million short tons, leaving the U.S share of global trade slightly above the prior 5-year average. U.S. soybean exports are forecast at 1.98 billion bushels, down 40 million from 2022/23 with strong competition from increasing South American production and limited gains in global import demand. U.S. ending stocks for 2023/24 are projected at 335 million bushels, up 120 million from the revised 2022/23 forecast. Soybean and product prices are all forecast lower for 2023/24. The 2023/24 U.S. season-average soybean price is forecast at $12.10 per bushel compared with $14.20 per bushel in 2022/23.

Wheat

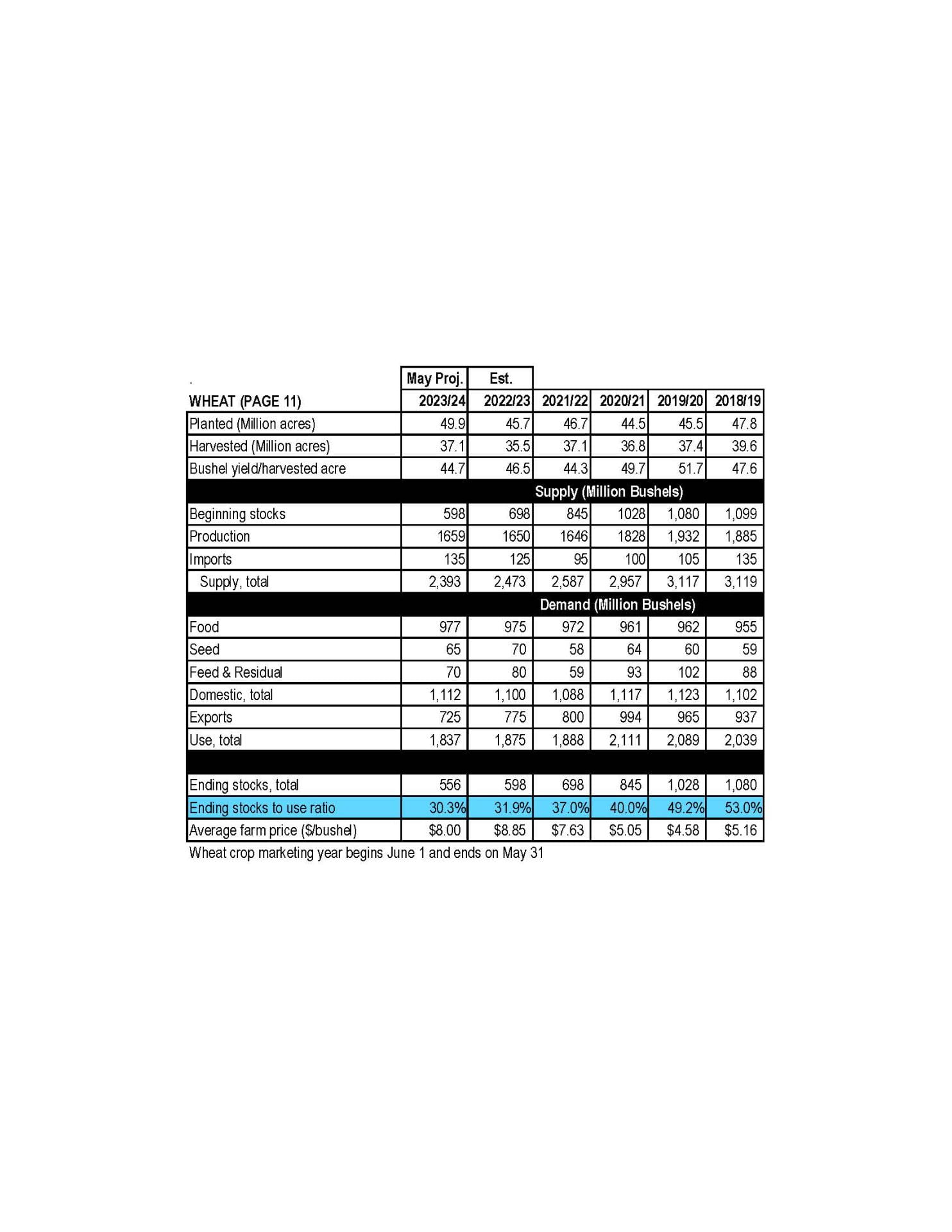

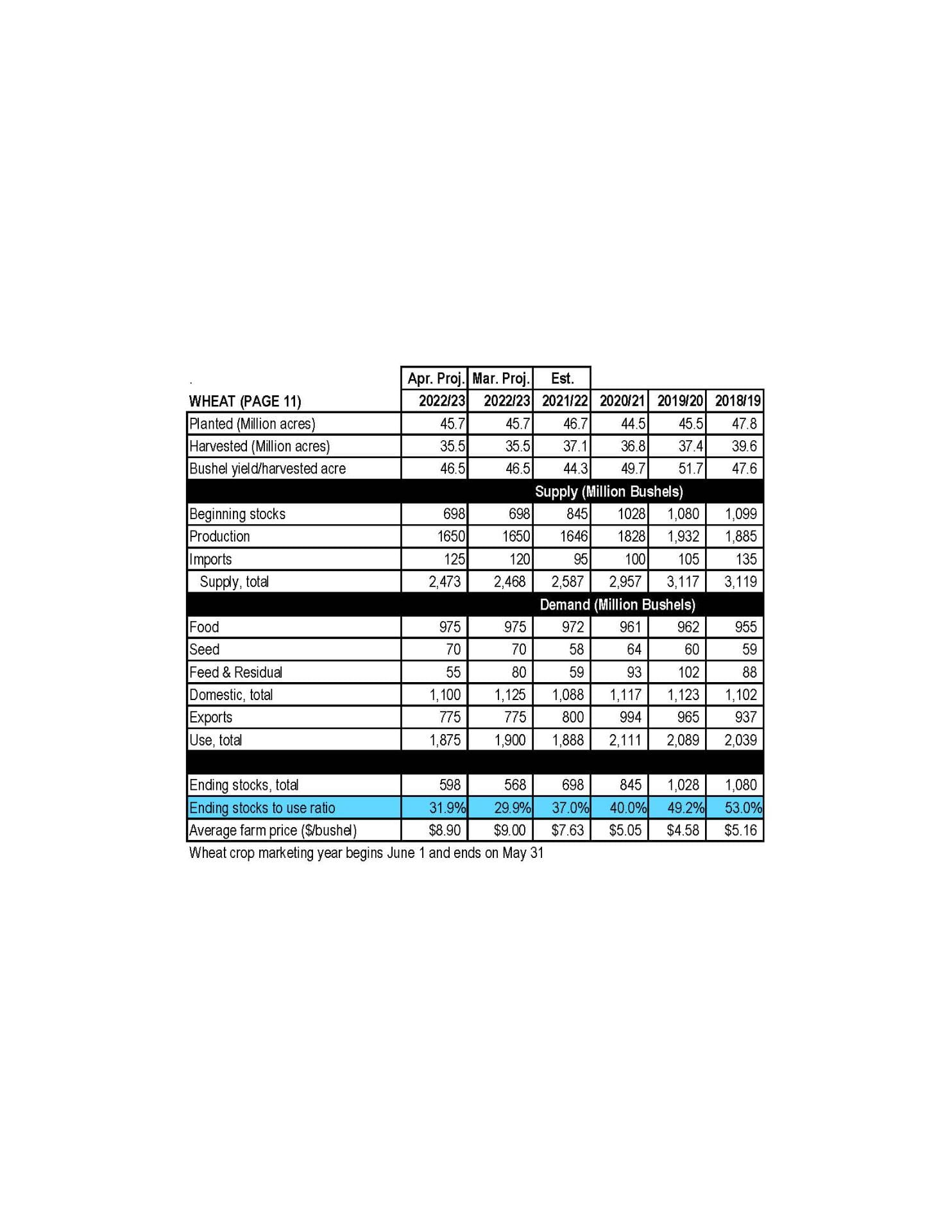

The 2023/24 outlook for U.S. wheat is for reduced supplies and exports, increased domestic use, and smaller stocks compared with 2022/23. U.S. wheat supplies are forecast lower than last year with smaller beginning stocks and only slightly larger production. All wheat production is projected at 1,659 million bushels, up modestly from last year on increased harvested area. However, the harvest-to-plant ratio is down from last year with above-average abandonment in Texas, Oklahoma, and Kansas. The all wheat yield, projected at 44.7 bushels per acre, is 1.8 bushels lower than last year. The first survey-based production forecast for 2023/24 winter wheat is up 2 percent from last year as higher Soft Red Winter production more than offsets a decline in Hard Red Winter and White wheat. Total 2023/24 domestic use is projected at 1,112 million bushels, up 1 percent from last year, primarily on increased feed and residual use. Exports are projected at 725 million bushels, 50 million lower than last year. Ending stocks are projected 11 percent lower than last year and the lowest in 16 years. The projected 2023/24 season-average farm price is $8.00 per bushel, down $0.85 from last year’s record.

Alyssa Koehler, Extension Field Crop Pathologist | akoehler@udel.edu University of Delaware

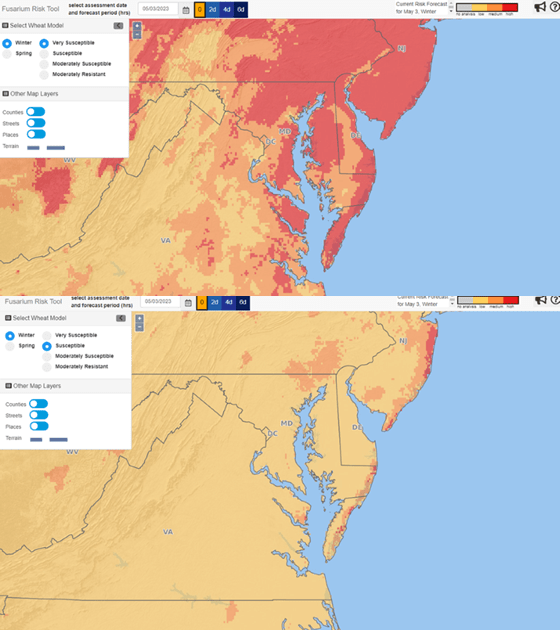

Wheat anthesis (flowering) is underway and will be continuing for the next 1-2 weeks across the region. Up until the rains this past weekend, we have been at low FHB risk. We are currently tracking as medium-high risk for very susceptible varieties and low-medium risk for varieties with some level of resistance (Figure 1). If you are planning for wheat fungicide application, scout frequently, looking for yellow anthers in the center of the wheat head (Figure 2) to signal that flowering has begun (Feekes 10.5.1). Depending on the weather, we can usually expect flowers to start showing up on wheat heads 3-5 days after full head emergence, with cool weather this can stretch this process out to 7-10 days. Anthers can remain attached after flowering, but become a pale white. For best mycotoxin (DON) control, it is better to be at flowering or a few days beyond than to spray too early when heads are not out yet (especially those secondary tillers). Fungicide products should be applied at the manufacturers recommended rate with nozzles angled 30-45° from horizontal (30 degrees is better than 45). Nozzles angled both forward and backward or twinjet nozzles that spray in two directions give better contact with the head and increase fungicide efficacy. For ground sprays, fungicides should be applied in at least 10-15 gallons of water per acre; aerial applications are recommended at 5 gallons per acre.

Figure 1. FHB Risk Model for very susceptible (top) and susceptible varieties (bottom) May 3, 2023 (wheatscab.psu.edu).Figure 2. Wheat at flowering (Feekes 10.5.1) with yellow anthers visible 3-4 days after heads emerge.

Once wheat has flowered, symptoms of FHB are usually visible in 18-24 days, but cool weather can slow symptom development. Heads with FHB will have bleached florets or bleached sections of the head and may have pink growth on spikelets. Glume blotch may also be present, but typically has more of a grey appearance. You can follow these steps to assess the severity of FHB present in your field.

For every 10 acres of field, randomly select one spot to survey.

Keeping your line of sight above the wheat heads, walk 40-50 yards and randomly pick 10-20 heads to look at on the plant or detach and place into a bag. (Looking down may bias the heads you select).

Once you have randomly collected the heads, rate the percent of each head with symptoms of FHB (bleaching or pink growth on spikelets). You can use the scale below to help calibrate your eye (next page).

After you have recorded values for each head, determine the average percent FHB severity by dividing the sum of disease severities by the total number of heads collected. (Ex. You rate 10 heads with severity values: 0%, 10%, 30%, 0%, 0%, 20%, 10%, 0%, 0%, 0%. These add up to 70. 70/10 heads = 7% overall FHB severity). Higher levels of FHB are typically associated with elevated levels of DON and possible issues with yield and test weight. It is possible to have delayed or lower levels of symptoms and still have DON.

Repeat this assessment as needed to get an overall rating for the field. Fields with greater than 10% FHB severity are at higher risk for yield losses or elevated DON. Fields with elevated DON should be harvested as early as possible and you may want to consider increasing combine fan speeds and shutter openings to reduce the amount of scabby kernels harvested.

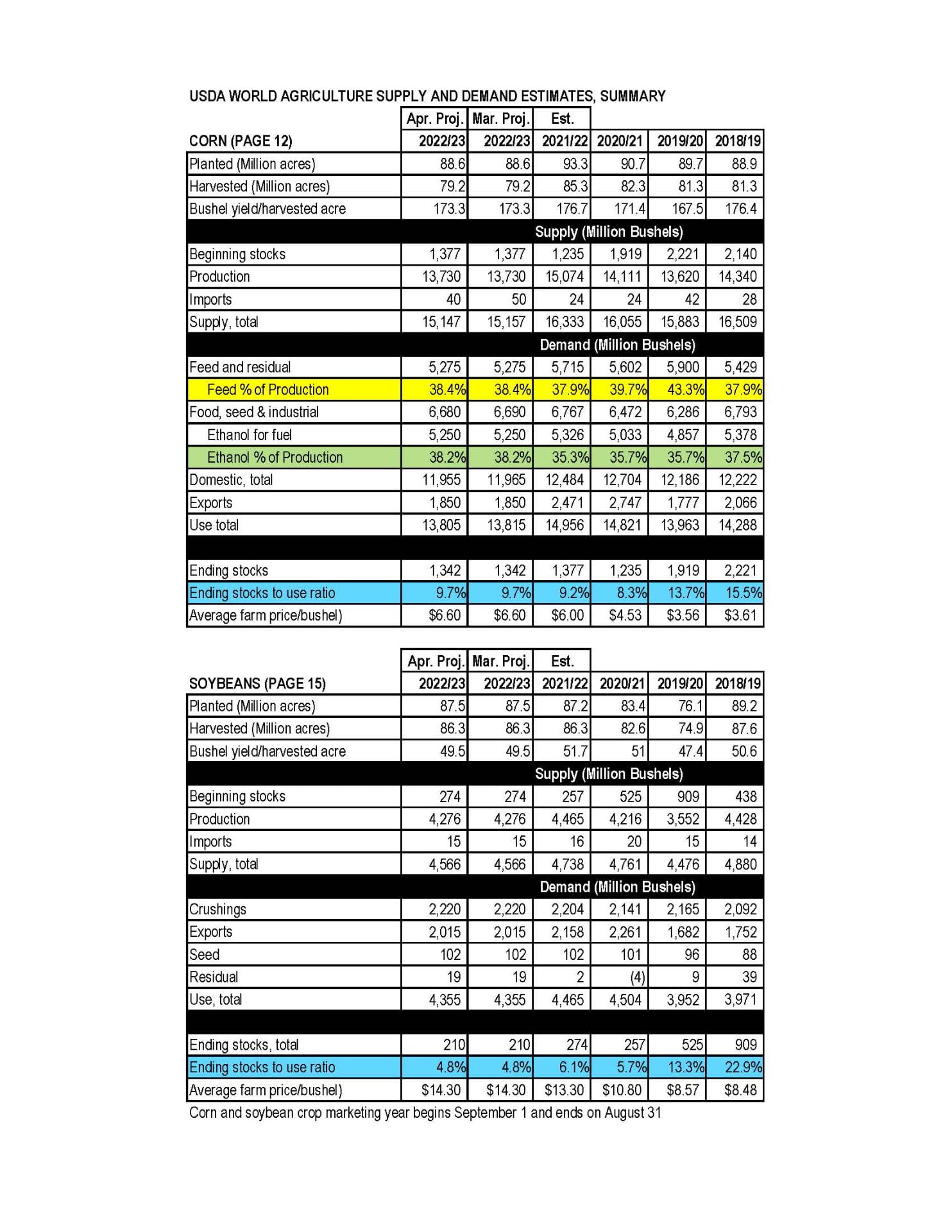

This month’s ‘22/23 U.S. corn outlook is for reductions to imports and food, seed, and industrial (FSI) use, with unchanged ending stocks. Corn imports are lowered 10 million bushels based on observed trade to date. Feed and residual use is unchanged at 5.275 billion based on indicated disappearance during the December-February quarter. FSI is lowered 10 million bushels reflecting cuts to corn used for glucose and dextrose and starch. With supply and use falling by the same amount, ending stocks are unchanged at 1.342 billion bu. The season-average price is unchanged at $6.60 per bu.

Soybeans

U.S. soybean supply and use forecasts for ‘22/23 are unchanged relative to last month. Soybean and soybean meal prices are also unchanged. The soybean oil price is projected at 64.0 cents per pound, down 2 cents. Global ‘22/23 soybean supply and demand forecasts include lower production, crush, and exports. Global soybean production is reduced 5.5 million tons to 369.6 million. Lower crops for Argentina and Uruguay are partly offset by higher production for Brazil. Soybean production for Argentina is lowered 6.0 million tons to 27.0 million on hot and dry weather conditions through March. Uruguay production is lowered 0.9 million tons to 1.2 million on a lower harvested area and yield. Partly offsetting is higher production for Brazil, increased 1.0 million tons to 154.0 million on higher area. Soybean crush is lowered on reduced supplies and slow pace to date for Argentina, China, Bangladesh, Pakistan, and Egypt. Crush for Argentina is reduced 3.3 million tons to 32.0 million leading to lower product exports. Partly offsetting is higher crush and higher soybean oil and meal exports for Brazil. Soybean exports are lowered 0.4 million tons to 168.0 million on lower exports for Uruguay. Imports are lowered for Bangladesh, Egypt, and Pakistan and raised for Argentina. Soybean ending stocks are raised fractionally with higher stocks for China and Brazil that are mostly offset by lower stocks for Argentina.

Wheat

The outlook for ‘22/23 U.S. wheat this month is for slightly higher supplies, reduced domestic use, unchanged exports, and increased ending stocks. Supplies are raised 5 million bushels on higher imports, based on the pace of Census imports reported to date. Domestic use is lowered 25 million bushels on reduced feed and residual use, which is decreased to 55 million. The downward revision is based on the implied disappearance for the second and third quarters indicated in the NASS Grain Stocks report. Wheat exports remain at 775 million bushels but there are offsetting by-class changes for White and Hard Red Spring exports. Projected ‘22/23 ending stocks are raised 30 million bushels to 598 million but are still 14% below last year. The ‘22/23 season-average farm price is forecast $0.10 per bushel lower at $8.90, based on NASS prices reported to date and expectations for cash prices for the remainder of ‘22/23. The global wheat outlook for ‘22/23 is for increased supplies, higher consumption, and reduced trade and stocks. Supplies are raised 0.7 million tons to 1,061.1 million, primarily on higher beginning stocks for Syria and increased production for Ethiopia. Global consumption is increased 2.9 million tons to 796.1 million, mainly on higher food, seed, and industrial use for India, and increased feed and residual use for China and the EU. World trade is lowered 1.2 million tons to 212.7 million on reduced exports by the EU, Argentina, and Brazil more than offsetting increases for Russia and Ukraine. China’s wheat imports are raised 2.0 million tons to 12.0 million, which would be the highest imports for China since 1995/96. China’s imports are raised on strong imports to date, particularly from Australia; China is now the leading 2022/23 global wheat importer. Projected 2022/23 world ending stocks are lowered 2.1 million tons to 265.1 million, the lowest since 2015/16. This month, India, the Philippines, and Ukraine are projected to have lower stocks, more than offsetting increases for Syria, the EU, and the United States.

Seyedali Hosseinrad, Nidhi Rawat, Nicole Fiorellino, and Vijay K. Tiwari Department of Plant Science and Landscape Architecture, University of Maryland, College Park

Fusarium Head Blight of wheat and barley

Fusarium head blight (FHB) is a severe fungal disease that affects small grains, wheat and barley. It is particularly problematic in regions with wet and warm springs, such as the Mid-Atlantic region. FHB is caused by several species of Fusarium, F. graminearum being the most common in the USA.

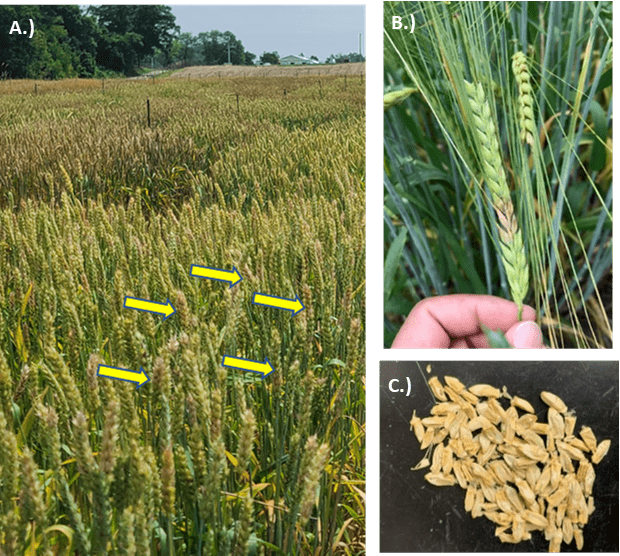

Symptoms and signs: The disease primarily attacks the wheat and barley heads, or spikes, at flowering. Early symptoms of FHB include the appearance of small, water-soaked lesions on the glumes and awns of the heads. As the infection progresses, these lesions become larger, and the spikelets (sections of the heads) become brown and dry progressively (Figure 1a, b). In particularly conducive weather conditions, the spikelets may take on a pink or reddish color due to a mass production of fungal spores called sporodochia on the glumes. The disease causes the kernels to shrink or abort, leading to reduced yield, poor-quality grain, and in severe cases, crop failure (Fig. 1 c). In addition, the fungus also produces mycotoxins, such as Deoxynivalenol (DON), which is toxic for human and animal consumption. The epidemiology of FHB is complex and multifaceted and can be influenced by various factors, including weather conditions, crop management practices, and genetic susceptibility.

Figure 1. FHB symptoms on wheat and barley. A.) Wheat heads showing brown and bleached spikelets indicated by yellow arrows. B.) A malting barley spike showing bleached spikelets. C.) Fusarium damaged kernels.

Factors affecting FHB

Weather conditions play a major role in determining the severity of FHB in field conditions. The disease thrives in warm, wet environments and is severe in areas with high humidity and frequent rainfall. Wet weather conditions during the flowering stage of wheat development provide an ideal environment for the fungus to infect and proliferate on the developing grain heads. In particular, warm and humid weather between heading and anthesis (flowering) is highly conducive to FHB infection. Warm temperatures between 70 and 80°F are favorable for fungal growth and production of mycotoxins.

Crop management practices can also contribute to the development and spread of FHB in winter wheat. Practices such as reduced tillage and corn-wheat rotation can increase the risk of FHB infection. Reduced or no-tillage can leave plant debris on the soil surface, providing a potential source of inoculum for the fungus. At the same time, corn acts as a secondary host of the pathogen, allowing the fungal inoculum to build up in the soil over time.

Management of FHB

Effective management of FHB in winter wheat typically involves using an integrated disease management approach that incorporates a combination of cultural, chemical, and biological control measures.

Use of FHB-resistant varieties: One of the most important cultural practices for reducing FHB infections in wheat is the selection of resistant cultivars. Several wheat varieties have been developed with genetic resistance to FHB. In fact, the UMD small grain pathology program, in collaboration with the small grain breeding program, tests upward of 60 regional commercial varieties in their misted nursery in replicated trials every year to provide growers with a robust assessment of the levels of the genetic resistance of these varieties to FHB (https://psla.umd.edu/extension/md-crops). It is highly advisable for regional farmers to refer to these ratings for making their planting decisions to reduce the severity of infections in their crops.

Due to the importance of FHB in the Mid-Atlantic region, developing FHB-resistant varieties is one of the primary goals of the MD small grain breeding program, in addition to their yield and quality. Resistance to FHB is a complex genetic trait and is influenced by a range of genetic factors. So, any breeding program targeting to incorporate a high level of genetic resistance in their varieties has to pyramid several genes toward that goal. However, a high level of genetic resistance in barley is difficult to achieve on account of the lack of resistance genes available in it.

Chemical control: The use of fungicides is a key component of FHB management in wheat and barley. Fungicides can effectively reduce the severity of infections and minimize the production of mycotoxins. Fungicides with Group 3 and 7 FRAC code ingredients have been successful in controlling FHB. FRAC group 11 fungicides should not be applied for FHB, as there are reports of them increasing DON content in the grains. Several effective chemistries with a mix of active ingredients against FHB have recently been released by manufacturers, such as Prosaro-Pro and Prosaro by Bayer, Miravis-Ace by Syngenta, and Sphaerex by BASF. All these fungicides have been tested by the UMD Small grain pathology program and are found to be equally effective when sprayed at anthesis.

In addition to the chemistry of the fungicide, the timing of spraying is very critical in managing FHB. Spraying fungicides at anthesis (when yellow anthers pop out of the wheat heads) in wheat and heading in barley is important. As weather plays a major effect in determining the severity of FHB infection, the risk of FHB can be predicted with a significant correlation with conducive weather conditions. In conjunction with the US Wheat and Barley Scab Initiative, the MD small grain program releases FHB risk commentaries for growers registered with the FHB risk prediction website (https://www.wheatscab.psu.edu/). The growers are advised to register on this website to receive the alerts on their cell phones as text messages with advice on spraying decisions for FHB.

Biological control: Some biological control agents, such as bacterial and fungal species antagonistic to FHB, are available with the claims of reducing disease severity and mycotoxin production. However, the efficacy of these biological control agents is not high yet. Researchers at UMD are testing some new promising biological products currently under development, especially for the organic growers of the region.

Crop Rotation and Tillage: Other important cultural practices include crop rotation and tillage. Planting non-host crops such as soybeans in rotation with wheat can help reduce the amount of FHB inoculum in the soil, as corn is a secondary host of the pathogen and can increase inoculum build-up in the soil for the wheat crop. Reduced tillage practices that manage crop residue on the soil surface with minimal disturbance to the soil are helpful in reducing the amount of infected crop residue on the soil surface while minimizing soil erosion and loss.

Post-harvest management: Post-harvest management practices, such as grain cleaning and drying, can help to screen the Fusarium damaged kernels that are expected to have high levels of mycotoxin contamination in the harvested grain. Cleaning equipment such as air screen cleaners or gravity tables can remove lightweight and damaged kernels. Drying grain to a moisture content of 14% or lower as soon as possible after harvest can also help minimize mycotoxin contamination. The fungus may continue mycotoxin production at high moisture conditions in storage. Proper storage conditions, such as cool and dry storage facilities, can also help to prevent mycotoxin contamination during storage.

Fusarium head blight (FHB) is a significant fungal disease affecting wheat and barley crops in the Mid-Atlantic region, causing yield and quality losses. Small grain pathology and breeding programs are working on multipronged approaches to reduce FHB impact, such as using fungicides, developing resistant cultivars, and adopting cultural practices such as crop rotation and tillage management. Also, research and innovation are crucial to ensure the region’s long-term sustainability of wheat production.

For more information:

Gillum, M., & Van Sanford, D. (2023). Understanding the Effect of Fusarium Head Blight Resistance on Agronomic Characteristics of Soft Red Winter Wheat.

Singh, L., Wight, J.P., Crank, J., Thorne, L., Erwin, J.E., Dong, Y., Rawat, N. (2021). Evaluation of application timing of Miravis-Ace for control of Fusarium head blight and DON content in wheat. Plant Health Progress. 22: 94-100.

Singh, L., Wight, J.P., Crank, J., Thorne, L., Dong, Y., Rawat, N. (2020). Efficacy assessment of a new fungicide, Miravis Ace, for control of

Attachedis the summary for the October 2022 WASDE.

Corn

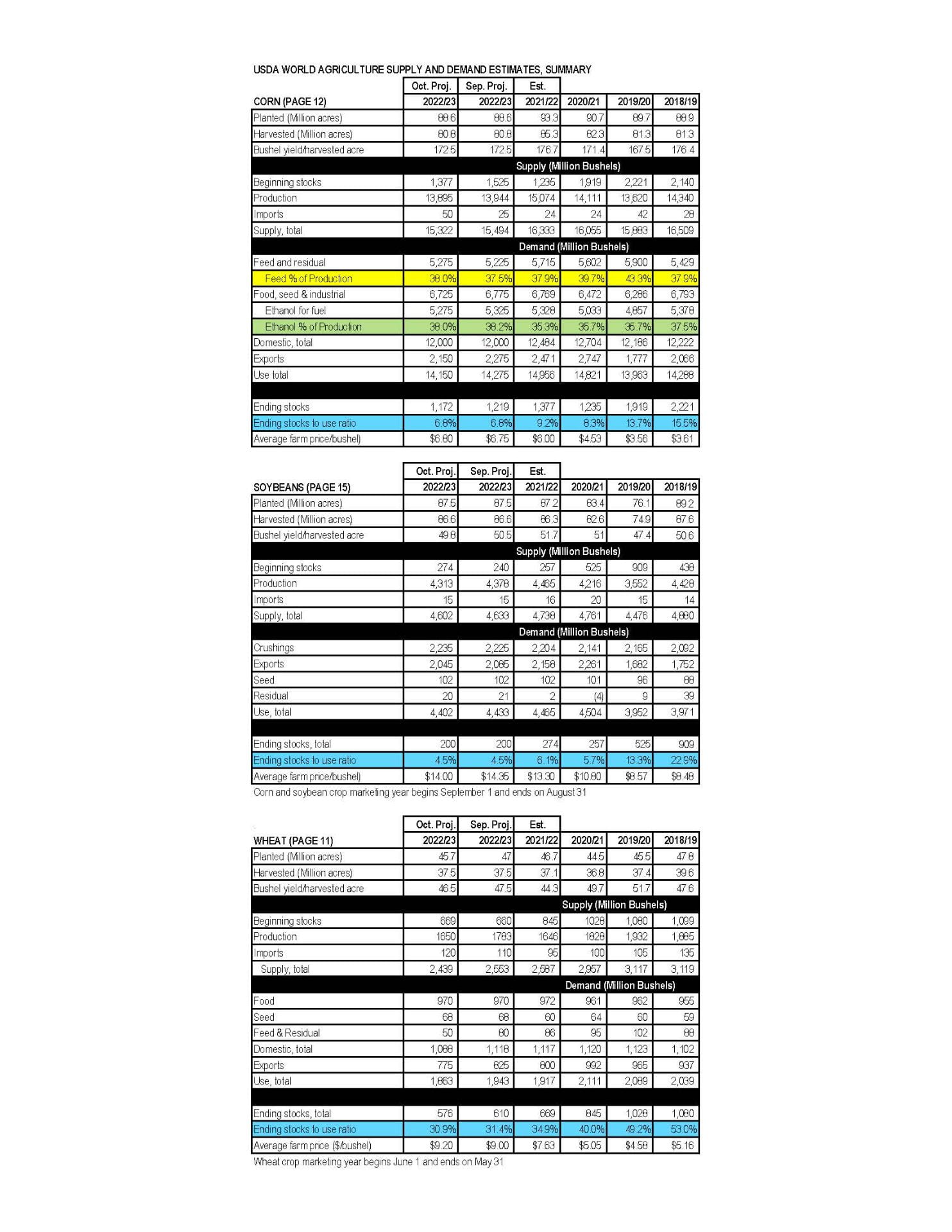

This month’s 2022/23 U.S. corn outlook is for reduced supplies, greater feed and residual use, lower exports and corn used for ethanol, and smaller ending stocks. Corn production is forecast at 13.895 billion bushels, down 49 million on a reduction in yield to 171.9 bushels per acre. Corn supplies are forecast at 15.322 billion bushels, a decline of 172 million bushels from last month, as lower production and beginning stocks are partially offset by higher imports. Exports are lowered 125 million bushels reflecting smaller supplies and slow early-season demand. Projected feed and residual use is raised 50 million bushels based on indicated disappearance during 2021/22. Corn used for ethanol is lowered 50 million bushels. With supply falling more than use, corn ending stocks for 2022/23 are cut 47 million bushels. The season-average corn price received by producers is raised 5 cents to $6.80 per bushel.

Soybeans

Soybean production is forecast at 4.3 billion bushels, down 65 million on lower yields. Harvested area is unchanged at 86.6 million acres. The soybean yield is projected at 49.8 bushels per acre, down 0.7 bushels from the September forecast. With lower production partly offset by higher beginning stocks,

supplies are reduced 31 million bushels. Soybean exports are reduced 40 million bushels to 2.05 billion with increased competition from South America. With lower exports partly offset by increased crush, ending stocks are unchanged from last month at 200 million bushels. The U.S. season-average soybean price for 2022/23 is forecast at $14.00 per bushel, down 35 cents.

Wheat

The outlook for 2022/23 U.S. wheat this month is for lower supplies, domestic use, exports, and stocks. Supplies are reduced on lower 2022/23 production based on the NASS Small Grains Summary that indicated reductions in both harvested area and yield. This lowered production by 133 million bushels to 1,650 million, leaving production only minimally higher than last year. Partially offsetting the production decline are higher projected imports, raised 10 million bushels to 120 million, all for Hard Red Spring. Annual feed and residual use is lowered 30 million bushels to 50 million, based on first quarter disappearance, as indicated in the NASS Grain Stocks report. This is the lowest first quarter total disappearance since 1983/84. Wheat exports are lowered 50 million bushels to 775 million on reduced supplies, slow pace of export sales, and continued uncompetitive U.S. export prices. This would be the lowest U.S. wheat exports since 1971/72. Projected ending stocks are lowered 34 million bushels to 576 million, which would be the lowest since 2007/08. The season-average farm price is raised $0.20 per bushel to $9.20 on reported NASS prices to date and expectations for futures and cash prices for the remainder of 2022/23.

Attachedis the summary for the September 2022 WASDE.

Corn

This month’s 2022/23 U.S. corn outlook is for lower supplies, smaller feed and residual use, reduced exports and corn used for ethanol, and tighter ending stocks. Projected beginning stocks for 2022/23 are 5 million bushels lower based on essentially offsetting export and corn used for ethanol changes for 2021/22. Corn production for 2022/23 is forecast at 13.9 billion bushels, down 415 million from last month on reductions to harvested area and yield. The national average yield is forecast at 172.5 bushels per acre, down 2.9 bushels. Harvested area for grain is forecast at 80.8 million acres, down 1.0 million. Total U.S. corn use is cut 250 million bushels to 14.3 billion. Feed and residual use is lowered 100 million bushels based on a smaller crop and higher expected prices. Exports are cut 100 million bushels to 2.3 billion while corn used for ethanol is lowered 50 million to 5.3 billion. With supply falling more than use, ending stocks are down 169 million bushels to 1.2 billion. The season-average corn price received by producers is raised 10 cents to $6.75 per bushel.

Soybeans

U.S. soybean supply and use changes for 2022/23 include higher beginning stocks and lower production, crush, exports, and ending stocks. Higher beginning stocks reflect a lower export forecast for 2021/22. Soybean production is projected at 4.4 billion bushels, down 152 million with lower harvested area and yield. Harvested area is down 0.6 million from the August forecast. The soybean yield forecast of 50.5 bushels per acre is down 1.4 bushels from last month. The crush forecast is reduced 20 million bushels and the soybean export forecast is reduced 70 million bushels on lower supplies. Ending stocks are projected at 200 million bushels, down 45 million from last month. The U.S. season-average soybean price is forecast at $14.35 per bushel, unchanged from last month. Soybean meal and oil prices are also unchanged at $390 per short ton and 69.0 cents per pound, respectively. Other changes this month include lower peanut and higher cottonseed production.

Wheat

The 2022/23 U.S. wheat outlook for supply and use is unchanged this month. The projected 2022/23 season-average farm price (SAFP) is lowered $0.25 per bushel to $9.00 on reported NASS prices to date and expectations for cash and futures prices the remainder of 2022/23. Despite the decline, $9.00 per bushel would remain a record SAFP.

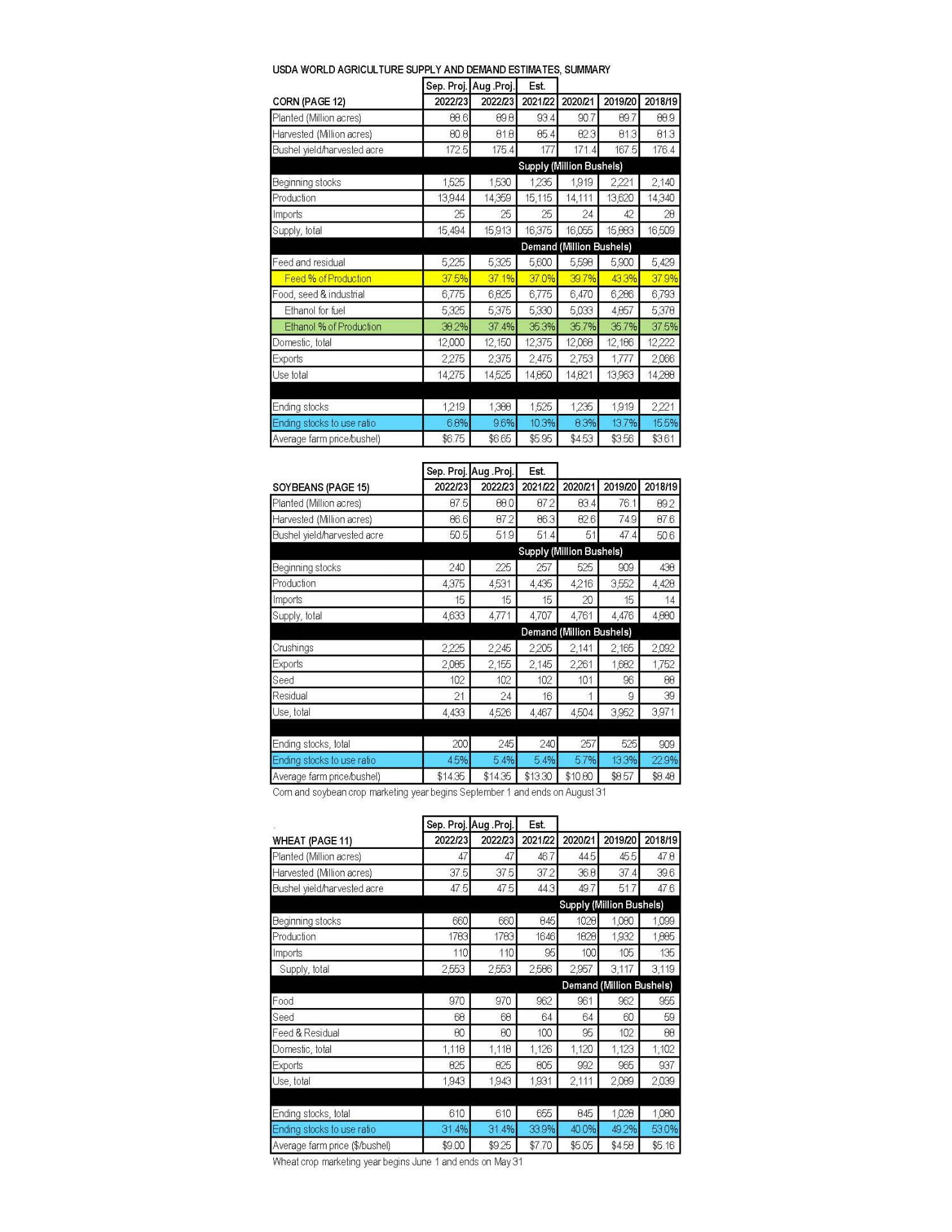

This month’s 2022/23 U.S. corn outlook is for lower supplies, reduced feed and residual use, slightly higher food, seed, and industrial use, smaller exports, and lower ending stocks. Projected beginning stocks for 2022/23 are 20 million bushels higher based on a lower use forecast for 2021/22, where a reduction in corn used for ethanol is partially offset by greater use for glucose and dextrose. Corn production for 2022/23 is forecast at 14.4 billion bushels, down 146 million from the July projection. The season’s first survey-based corn yield forecast, at 175.4 bushels per acre, is 1.6 bushels below last month’s projection. Among the major producing states, today’s Crop Production report indicates that yields are forecast above a year ago in Illinois, Minnesota, and South Dakota. Yields in Indiana, Missouri, Nebraska, and Ohio are forecast below a year ago. Iowa is unchanged. Total U.S. corn use for 2022/23 is reduced 45 million bushels to 14.5 billion. Feed and residual use is lowered 25 million bushels based on a smaller crop. Corn used for glucose and dextrose is projected higher based on observed use during 2021/22. Exports for 2022/23 are cut 25 million bushels to 2.4 billion. With supply falling more than use, ending stocks are lowered 82 million bushels to 1.4 billion.

Soybean

U.S. soybean supply and use changes for 2022/23 include higher beginning stocks, production, exports, and ending stocks. Beginning soybean stocks are raised on lower 2021/22 exports. Soybean production for 2022/23 is forecast at 4.53 billion bushels, up 26 million with higher yields more than offsetting lower harvested area. Harvested area is forecast at 87.2 million acres, down 0.3 million from July. The first survey-based soybean yield forecast of 51.9 bushels per acre is raised 0.4 bushels from last month. Soybean supplies for 2022/23 are projected at 4.8 billion bushels, up 36 million from last month. U.S. soybean exports are raised 20 million bushels to 2.16 billion on increased supplies. Soybean ending stocks are forecast at 245 million bushels, up 15 million.

Wheat

The outlook for 2022/23 U.S. wheat this month is for increased supplies, higher domestic use and exports, and reduced stocks. Supplies are raised on higher production with all wheat production forecast at 1,783 million bushels, up 2 million from last month. Reductions in winter wheat and Durum are more than offset by an increase in Other Spring Wheat. The all wheat yield is 47.5 bushels per acre, up 0.2 bushels from last month. Food use is raised 6 million bushels to 970 million, based primarily on the NASS Flour Milling Products report, issued August 1. The report indicated record wheat flour millings in the April-June quarter, which resulted in raising 2021/22 food use to a record 972 million bushels. Wheat exports for 2022/23 are increased 25 million bushels to 825 million with most of the upward adjustment for Soft Red Winter and White, based on competitive export prices. Projected 2022/23 ending stocks are lowered 29 million bushels to 610 million.

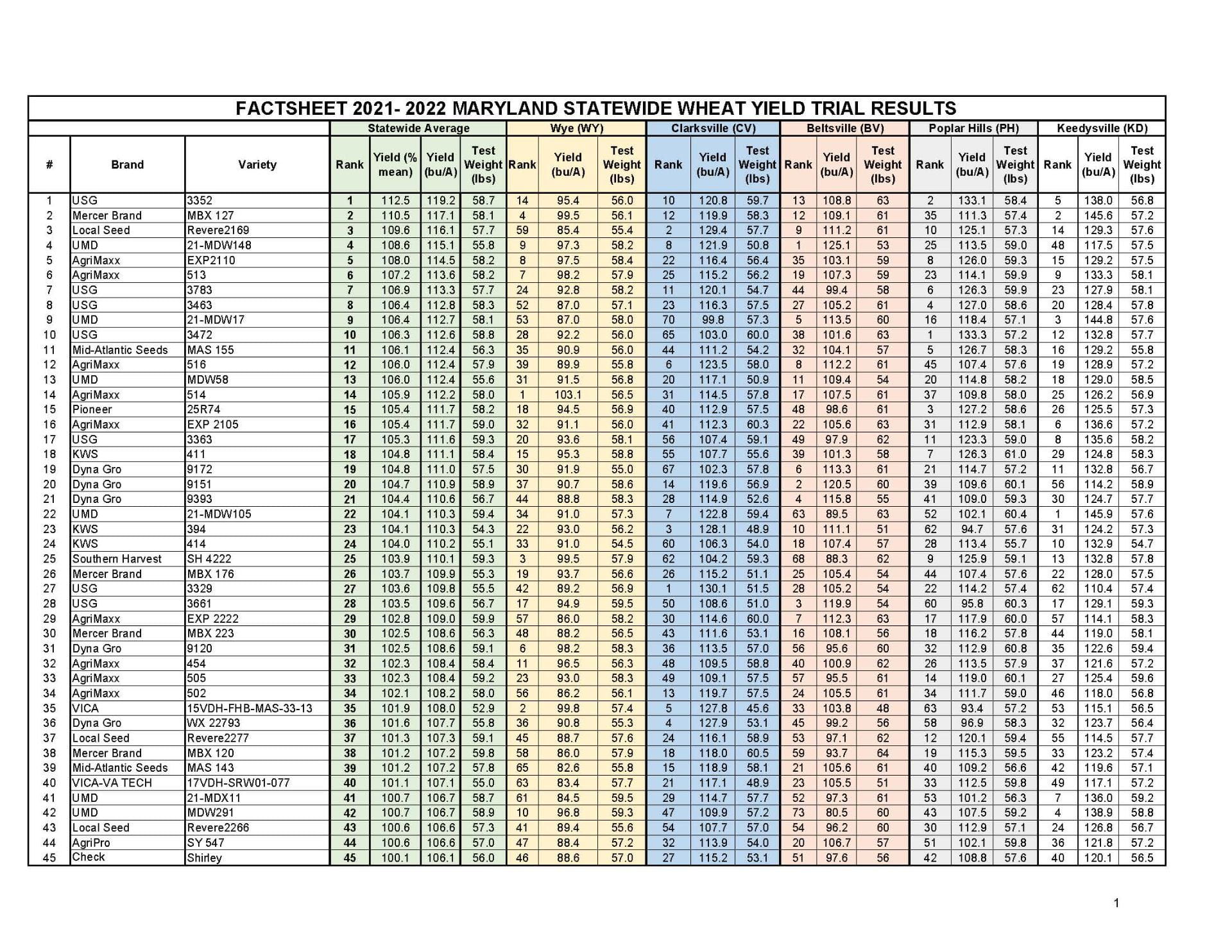

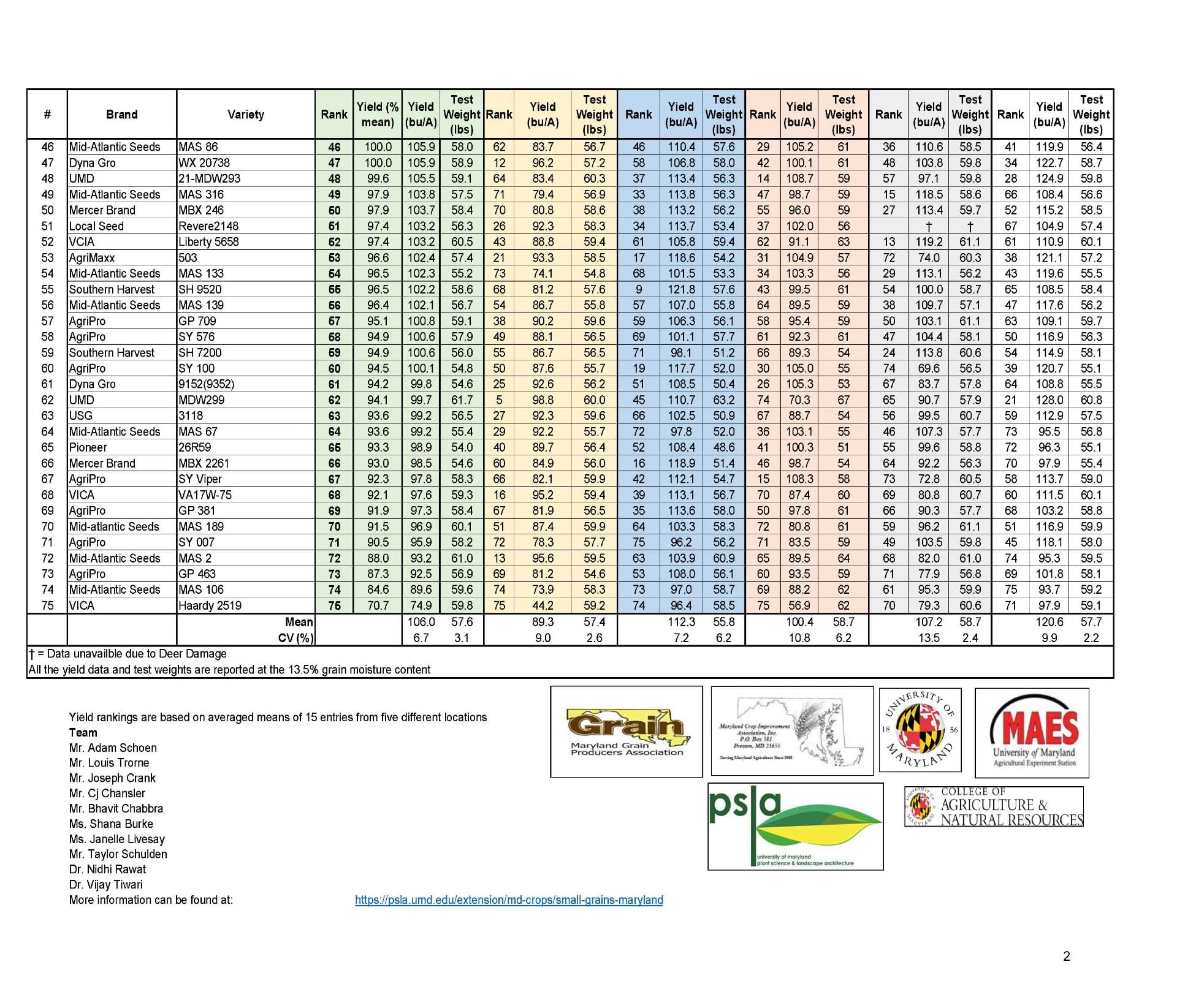

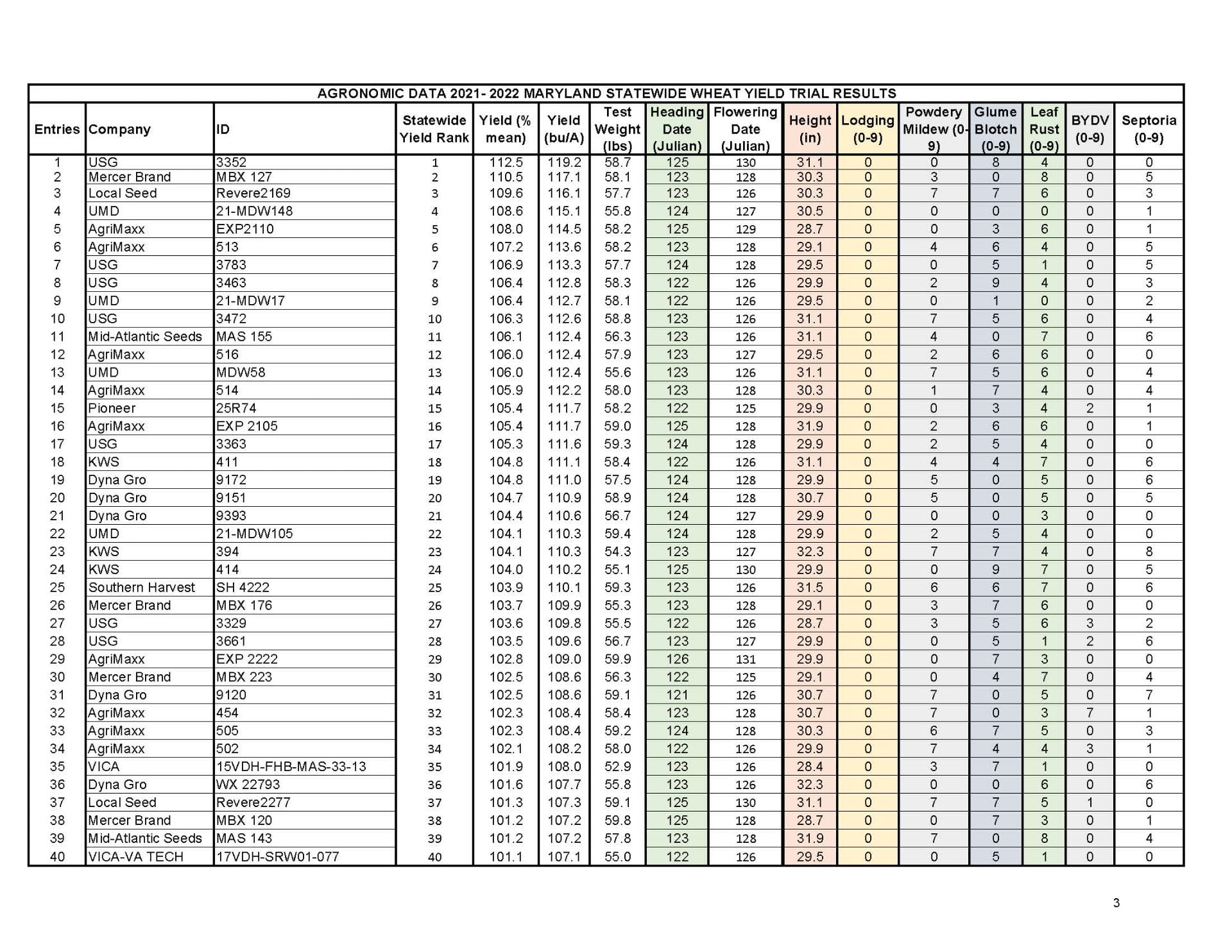

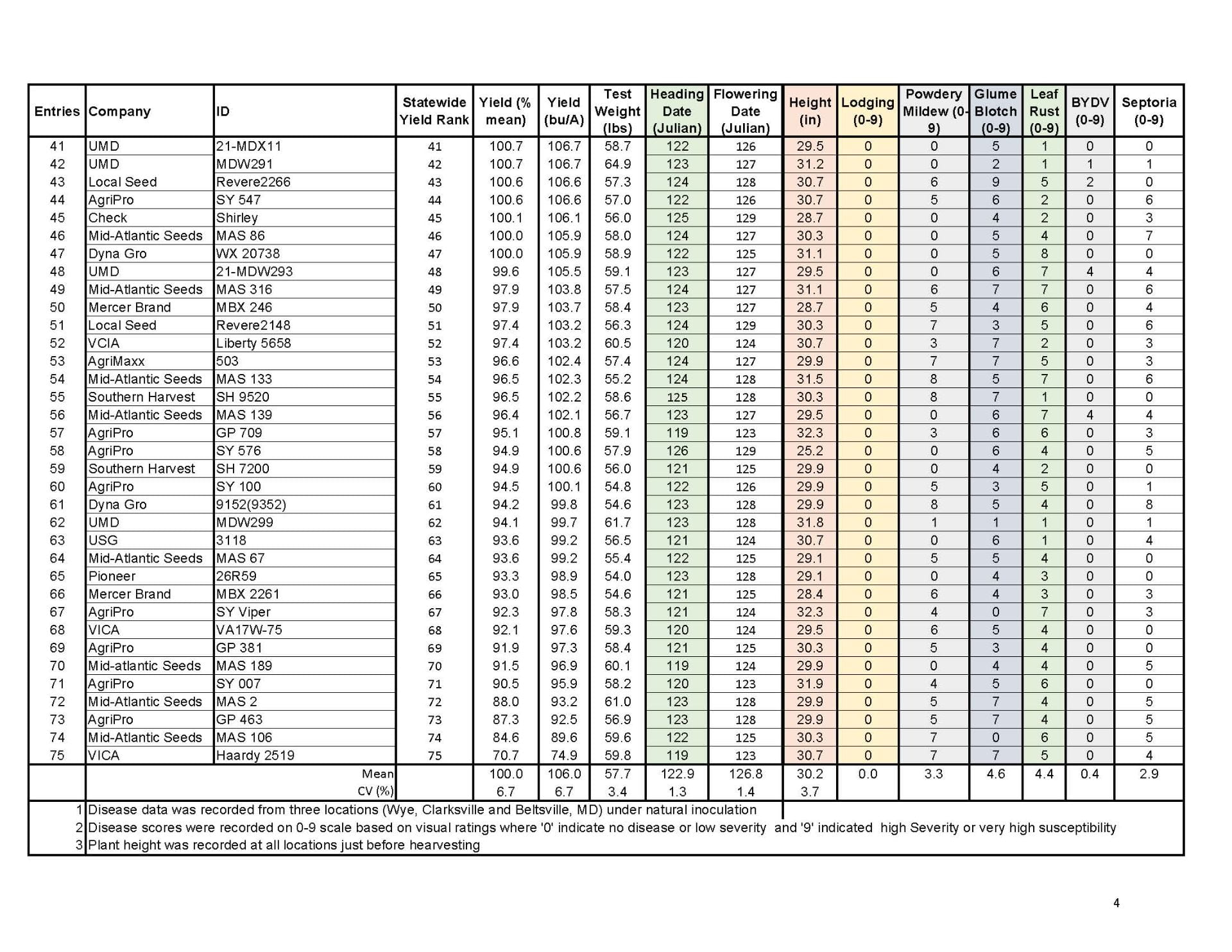

Results from the University of Maryland Small Grain Variety Trials are in the tables below. To download a pdf copy of the report, click here.

University of Maryland also rates the relative susceptibility of select varieties of wheat and barley to Fusarium head blight. The results from this trial can be found here.

For questions regarding the small grain trials, contact Dr. Vijay Tiwari (vktiwari@umd.edu) or Dr. Nidhi Rawat (nidhirwt@umd.edu).

If you’d like to learn more about how to interpret variety trial data, view our fact sheet by clicking here.

This month’s 2022/23 U.S. corn outlook is for larger beginning stocks, slightly higher use, and increased ending stocks. Corn area and yield forecasts are unchanged. USDA will release its acreage report on June 30, which will provide survey based indications of planted and harvested area. Beginning stocks are up 45 million bushels mostly reflecting a forecast decline in exports for 2021/22. Exports are lowered 50 million bushels, based on reported U.S. Census Bureau shipments through the month of April and export inspection data for the month of May. Food, seed, and industrial use (FSI) is raised 5 million bushels as projected increases in the amount of corn used for glucose and dextrose and starch is partially offset by a decline in high fructose corn syrup. These FSI use changes are carried through for 2022/23. With no other 2022/23 use changes, ending stocks are raised 40 million bushels. The season-average farm price received by producers is unchanged at $6.75 per bushel.

Soybeans

This month’s U.S. soybean supply and use projections for 2022/23 include lower beginning and ending stocks and higher prices. Lower beginning stocks reflects increased exports for 2021/22. Soybean exports for 2021/22 are raised 30 million bushels to 2.17 billion reflecting strong export sales and a reduced export forecast for Brazil. With reduced supplies for 2022/23 and no use changes, soybean ending stocks are projected at 280 million bushels, down 30 million. The soybean price is forecast at $14.70 per bushel, up 30 cents from last month.

Wheat

The outlook for 2022/23 U.S. wheat this month is for increased supplies, unchanged domestic use and exports, and higher stocks. Supplies are raised on higher production with all wheat production projected at 1,737 million bushels, up 8 million from last month. NASS raised winter wheat production to 1,182 million bushels as increases for Soft Red Winter and White Winter more than offset a reduction for Hard Red Winter. The all wheat yield is 46.9 bushels per acre, up 0.3 bushels from last month. Projected 2022/23 ending stocks are raised 8 million bushels to 627 million, still down 4 percent from 2021/22. The projected 2022/23 season-average farm price is unchanged at $10.75 per bushel, compared to $7.70 for 2021/22.

Andrew Kness, Agriculture Agent | akness@umd.edu University of Maryland Extension, Harford County

In general, the wheat crop is looking pretty good across the region, but there have been some not-so-good looking fields. This spring’s abnormal weather patterns have lead to some interesting symptom development in wheat. In my travels across the county and state and in conversations with colleagues in the area, several wheat fields have been exhibiting disease-like symptoms that are not readily attributed to any one disease.

Figure 1. Symptomatic wheat plants.

The symptoms include general yellowing of plants, yellow leaf tips, and/or flecking on the leaves (Figure 1). The flecking on the leaves is a symptom that can be caused by many different biotic and abiotic factors, but when entire fields are affected it is generally associated with a condition called physiological leaf fleck (Figure 2). Leaf flecking can be caused by periods of cloudy weather followed by bright, sunny weather, which we have certainly had this spring. However, similar symptoms can also be associated with viral infections and bacterial pathogens. Bacterial infections in wheat are not very common in our region; however, wheat samples in nearby Delaware tested positive for the bacterial wheat pathogen, Clavibacter michiganensis subsp. tessellarius (Cmt, Figure 3). Both physiological leaf fleck and Clavibacter m. tessellarius are believed to have little-to-no impact on yield.

Figure 2. Symptoms of physiological leaf flecking.

A second disease that we are seeing associated with these yellowing leaf tip symptoms is Barley Yellow Dwarf Virus (BYDV) and Cereal Yellow Dwarf Virus (CYDV). Both viruses have similar disease cycles and are vectored by aphids, primarily in the fall. What is interesting is that BYDV symptoms are typically also associated with bronzing of the leaf tips; however, these particular wheat samples did not exhibit these classic symptoms. Additionally, some plants that were exhibiting bronzing/purple leaf tips did not test positive for BYDV or any other viral pathogens, which leads me to this takeaway point—disease symptoms in wheat can be very tricky to decipher, especially when weather events complicate symptom expression. Wheat can be particularly sensitive to freeze, cold, and even sunny weather events in the spring, especially if weather conditions fluctuate. In many cases, symptom expression in response to environmental stressors can mask, uncover, or mimic disease issues. Furthermore, disease symptoms are not always “textbook,” so relying on visual identification is not enough to properly diagnose problems.

Figure 3. Wheat sample that tested positive for BYDV, CYDV, and Cmt.

Moving forward with wheat cultivation, it is important to keep this information in the back of your mind as you troubleshoot symptoms, and it is a good idea to utilize all the resources at your disposal, such as crop consultants, labs, and Extension professionals, to help diagnose problems.